Currencies + Interest Rates Mid-Year Video Update 2021

by WaveTrack International| August 10, 2021 | No Comments

Currencies + Interest Rates Mid-Year Video Update 2021 | PART III/III

US$ Dollar’s Long-Term Trend Remains Downwards basis 15.6-Year Cycle – Shorter-Term Correction unfolding Higher Since January and Set to Continue until October/November – Euro/US$ Corrective Downswing to 1.1320+/- with all G10’s in Corresponding Corrections – Commodity Currencies set to Weaken during Next Several Months – Asian Currencies in US$ Dollar Corrections – Interest Rates Finishing Counter-Trend Downswings but Risks of Continuation – Inflation TIPS in Correction – Spreads indicate new Widening Phase has begun in Dollars and Euros – Italy’s Yields still Trending Lower – Japan’s JPY10yr Continuing Lower.

INCLUDES ANALYSIS ON MAJOR US$ DOLLAR PAIRS/CROSSES – ASIAN/EM CURRENCIES – MEDIUM-TERM CYCLES – LONG-DATED YIELDS US/EUROPE/JAPAN + SPREADS

We’re pleased to announce the publication of WaveTrack’s Mid-Year 2021 trilogy video series of medium-term ELLIOTT WAVE price-forecasts. Today’s release is PART III, CURRENCIES & INTEREST RATES – Parts I & II were released during the last month – see below for information.

• PART I – STOCK INDICES – out now!

• PART II – COMMODITIES – out now!

• PART III – CURRENCIES & INTEREST RATES – out now!

Review – H1 2021

Economies have reopened after lengthy lock downs last year. Starting with an initial growth rebounding by double-digits as pent-up demand flows through order books in manufacturing and more recently, the services industry. This year’s numbers have been accompanied by surging inflationary pressures which reached peaks last March (2021). Although at the time, financial markets were positioning for continued price rises, interest rate rises and a weakening US$ dollar. However, the reality was quite the opposite.

In this year’s annual report, we commented – ‘…we know that such statistics can be misleading when it comes to timing imbalances that eventually lead to directional change, but sentiment data like this can be used in conjunction with Elliott Wave analysis which we can confirm shows that dollar oversold condition is about to change with significant corrective rallies already underway. The US$ dollar index is forecast up to 95.85+/- over the next 5-6 months, maybe even higher’.

US$ Dollar Index Performance

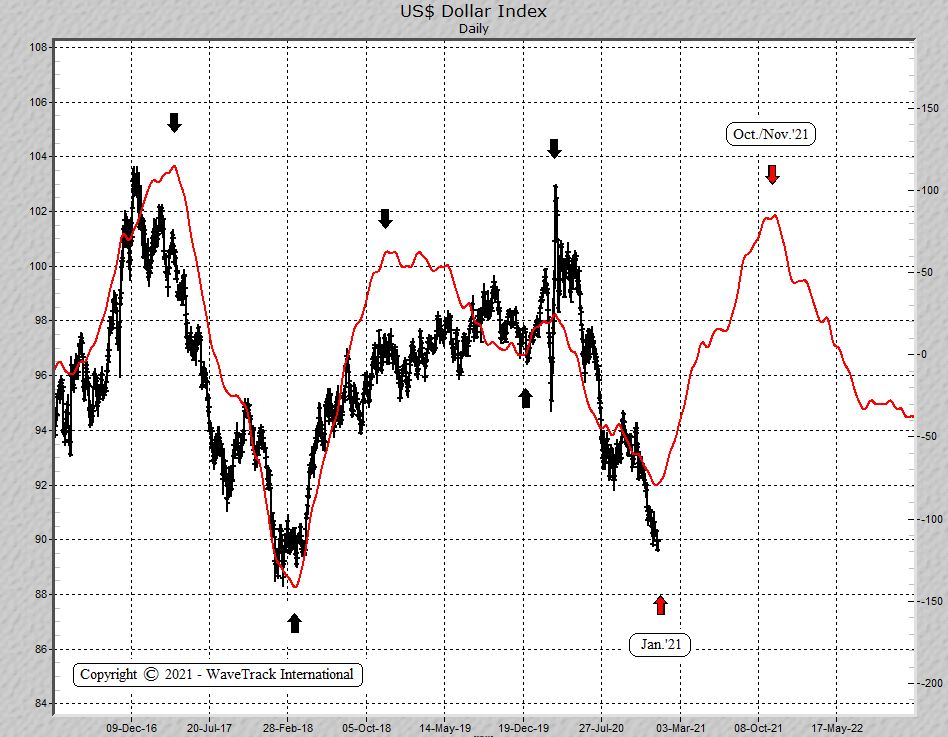

The US$ Dollar Index has certainly put in a base-line low last January at 89.21 and it’s been engaged in a counter-trend rally since, trading so far to 93.43. This rally is far from over, where upside targets of 95.85+/- are little changed, currently at 96.15+/-.

Interest Rates Performance

And for Interest Rates, a pause in those inflationary pressures was forecast basis analysis in the US10yr treasury yield and the Inflation TIPS, commenting – ‘…Whilst the long-term trends show a new 30+ year uptrend cycle for global interest rates, including treasury yields began from before last year’s COVID-19 pandemic lows, it is due to take a breather over the next 5-6 months…It’s necessary for a counter-trend 2nd wave downswing to now unfold. This suggests a temporary unwinding of the ‘Reflation-Trade’.

Exactly right! – the US10yr yield hit a peak last March at 1.774% per cent and has since traded down to .131%. So what can we expect next?

EW-Forecasts H2 2021

A lot of the normal correlations between the different asset classes have broken down this year. At the time of major turning points last year, in March’s ’20 pandemic highs/lows, the US$ Dollar hit a peak at 102.99 whilst stock markets like the benchmark S&P 500 traded to a low of 2191.86. The US$ dollar then declined into a five wave impulse pattern, ending last January ’21 at 89.21 and since trading higher into a correction. Yet, U.S. stock indices have yet to complete their corresponding advances although they’re expected at the end of August. But that means the normal correlation between these two asset classes have diverged for almost 8 months – see Fig #1.

Fig #1 – US Dollar Index – Composite Cycle – Monthly by WaveTrack International

Interest Rates

Interest rates bottomed into the March ’20 pandemic lows too with the US10yr yield hitting historical lows of 0.378% whilst the S&P 500 hit lows at 2191.86. But again, this relationship began to break down last March when the US10yr yield ended a its uptrend at 1.774 then declined earlier this month to 1.131 even though the S&P 500 has kept trending higher.

There’s also been a disruption in the way rising inflationary pressures have unfolded this year, in 2021. Investors surveyed last April by Bank of America showed 93% per cent were expecting the continuation of inflationary pressures – since then, rising food and agriculture prices (see PART II Commodities Report here) have exacerbated inflationary perceptions with lagging gains but with treasury yields declining over the past four months. However, that sentiment figure has now dropped to only 22% per cent.

The real difficulty in price forecasting is this divergence in ‘normal’ correlations. When they break down, it’s sometimes tricky to know how deep corrections can unfold if comparisons are removed from the equation – see Fig #1 – #2. This means that Elliott Wave patterns must be relied upon even if it sometimes doesn’t make sense.

Fig #2 – Corporate 30yr Bond Yield – Cycle Analysis by WaveTrack International

What would happen next if interest rates bottom now completing those corrections?

Is that bullish or bearish for stock markets? And the next direction for stock markets remains critical in forecasting the US$ dollar’s next moves. Hypothetically, should stock markets correct by -30% per cent, as we see a heightened risk, that certainly translates into a higher US$ dollar but what about interest rates? Do they attract safe-haven buying, consistent with historical precedent? Or do interest rates surge higher because of another round of rising inflationary pressures, sending stock markets lower. You see the point – the recent breakdown in correlations makes it difficult to be sure.

Of all the movements in stock markets, commodities, currencies and interest rates, we can say with confidence that the US$ dollar is rated as the highest outcome basis the current Elliott Wave analysis depicting January’s correction continuing higher until October/November.

We’re updating some amazing Elliott Wave forecasts for Currencies and U.S. interest rates, US30yr, US10yr, US05yr and even US02yr together with a schematic look at several spread relationships with European rates not forgetting upside targets for the US10yr Inflation Tips and our attempt to solve this financial riddle – it’s a must-see!

We invite you to take this next step in our financial journey with us – video subscription details are below – just follow the links and we’ll see you soon!

Most sincerely,

Peter Goodburn

Founder and Chief Elliott Wave Analyst

WaveTrack International

What you get!

Contents: 127 charts | VIDEO DURATION: 2 hours 34 mins.

The contents of this CURRENCY & INTEREST RATES VIDEO include Elliott Wave analysis for:

Currencies (92 charts):

• US$ Index + Cycles

• Euro/US$ + Cycles

• Stlg/US$

• US$/Yen

• US$/CHF

• US$/NOK

• US$/SEK

• AUD/US$

• US$/CAD

• NZD/US$

• Euro/Stlg

• Euro/CHF

• Euro/NOK

• Euro/Yen

• Euro/AUD

• Euro/CNY

• Stlg/YEN

• Stlg/CHF

• Stlg/NOK

• Stlg/ZAR

• Stlg/AUD

• AUD/NOK

• CAD/NOK

• AUD/CAD

• AUD/NZD

• Asian ADXY

• US$/Renminbi

• US$/KRW

• US$/SGD

• US$/INR

• US$/TWD

• USD/THB

• US$/MYR

• US$/IDR

• US$/PHP

• USD/BRL

• USD/RUB

• US$/ZAR

• US$/MXN

• US$/TRY

• US$/PLZ

• Bitcoin

• Ethereum

Interest Rates (37 charts):

• US30yr Yield + Cycles

• US10yr Yield + Cycles

• US5yr Yield

• US2yr Yield

• US2yr-10yr Yield Spread

• US10yr-30yr Yield Spread

• 3mth EuroDollar-US10yr Yield Spread

• Comparison US10-DE10yr vs S&P 500

• US10yr TIPS Break Even Inflation Rate

• US10-DE10yr Yield Spread

• DE10yr Yield

• ITY10yr Yield

• JPY10yr Yield

How to buy the Currencies + Interest Rates Mid-Year Video Update 2021

Simply contact us @ services@wavetrack.com to buy the CURRENCIES + INTEREST RATES Video Outlook 2021 for USD 48.00 (+ VAT where applicable) or alternatively our Triple Video Offer for USD 96.00 (+ VAT where applicable) – Review the content of WaveTrack Stock Indices Video PART I here and the Commodities Video PART II here.

*(additional VAT may be added depending on your country – currently US, Canada, Asia have no added VAT but most European countries do)

VIMEO – For clients who wish to purchase our video directly online – the video will be available within this week on VIMEO! We will publish the vimeo link here and on our twitter account!

We’re sure you’ll reap the benefits – don’t forget to contact us with any Elliott Wave questions – Peter is always keen to hear you views, queries and comments.

Visit us @ www.wavetrack.com

New Video! COMMODITIES CORRECTION AHEAD

by WaveTrack International| July 14, 2021 | No Comments

COMMODITY CORRECTION AHEAD’ – ‘PAUSE WITHIN INFLATION-POP’ CYCLE

We’re pleased to announce the publication of WaveTrack’s annual 2021 mid-year video updates of medium-term ELLIOTT WAVE price-forecasts. Today’s release is PART II, COMMODITIES – Part I was released last month and Part III will be published in late-July

• PART I – STOCK INDICES – out now!

• PART II – COMMODITIES – out now!

• PART III – CURRENCIES & INTEREST RATES – coming soon!

What is the Commodity Super-Cycle?

The Commodity Super-Cycle beginning from the Great Depression lows of year-1932 ended in 2006-08. Since then, a multi-decennial corrective downswing has begun a new deflationary era but with pockets of rising inflationary pressures.

Commotidies – Rising Inflationary Pressures

One of those pockets of rising inflationary pressures resumed in early 2016 but gained pace this year in 2021. However, it is set to surge higher through to a final peak due in 2023/24. This is the final phase of the ‘Inflation-Pop’ cycle.

But like all uptrends, including inflation, they are punctuated by intervening corrections – one of those corrections is set to begin NOW! Commodities have traded exponentially higher since the pandemic low of March ’20 but have reached interim upside price levels. Especially, since sentiment is euphoric whilst Elliott Wave patterns show a uniform completion to last year’s advances. This can be seen in Base Metals, Energy but also in Agriculture and Food. A 6-month correction lies directly ahead. Only afterwards does the inflation/price uptrends resume through 2022/2024.

Base Metals

A 6-month corrective downswing is about to get underway. Copper and Aluminium have seen the far greater advances from the pandemic lows of March ’20 relative to the other base metals. Copper has just completed its intermediate degree 3rd wave uptrend with a 4th wave correction of -29% per cent underway. Aluminium is approaching a peak for primary wave A with wave B’s correction -24% per cent set to begin. Lead is completing its 1st wave uptrend with a significant corrective pullback set to begin lasting through year-end, a decline of minimum -18% per cent. More about Zinc, Nickel and Tin prices in our latest EW-Commodities Video!

Base Metal Miners

The benchmark XME Metals & Mining index (ETF) is engaged in a five wave diagonal uptrend from the 2016 lows. A correction is expected over the next several months within its 3rd wave of -40% per cent. WaveTrack’s Commodities Video contains Elliott Wave charts of BHP Billiton, Freeport McMoran, Antofagasta, Anglo American, Kazakhmys Copper, Glencore, Rio Tinto, Teck Resources and Vale explaining in details what the next price move might be.

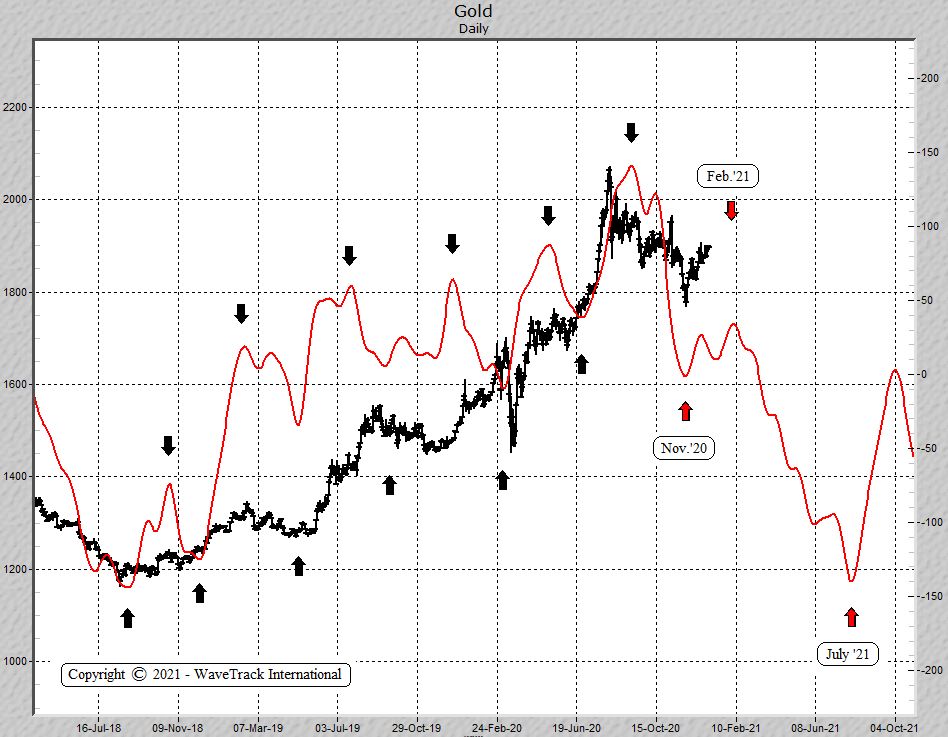

Precious Metals

Gold is set to continue trading lower from last August’s high of 2072.12 as part of primary wave 4’s correction. Downside targets remain towards 1600.00+/-. Gold continues to trade in negative-correlation to the US$ dollar index which is itself pushing higher from January’s low into a corrective rally, lasting into October/November. Longer-term upside targets remain towards 2472.00+/-. Silver continues to trade into a sideways 4th wave triangle from last August’s high of 29.86 – next downside targets remain towards 21.74+/-. Longer-term, upside targets remain towards 38.60+/-. Alternate counts are more bullish, towards 65.75+/-. Get insights into Platinum and Palladium forecasts in WaveTrack’s EW-Commodities Video.

Precious Metal Miners

The benchmark GDX Gold Miners index continues its corrective decline from last August’s high of 45.78 – downside targets towards 27.87+/-. XAU Gold/Silver index is set to extend last year’s correction targeting levels towards min. 116.17+/-, max. 109.37+/-. This corrective theme is repeated for many other gold and silver miners including Newmont Mining, Barrick Gold, Agnico Eagle, AngloGold Ashanti and Fresnillo Silver. More information about the Precious Miners long-term outlook can be found in this latest EW-Commodities Video!

Energy

The star performers in the commodity sector have been Crude and Brent oil. More about Crude Oil, Brent oil, XLE Energy and XOP Oil & Gas indices prices in our latest EW-Commodities Video!

Monetary & Fiscal Stimulus

Monetary and fiscal stimulus remains at unprecedented historical levels – the U.S. leads the world in both aspects – the Federal Reserve has bought $982 billion of mortgage bonds since March 2020, and currently plans to keep buying at least $40 billion each month. Those purchases, along with the Fed’s monthly purchases of $80 billion of treasury debt aims to hold down long-term borrowing costs to stimulate the economy as it recovers from the effects of the pandemic. See graphics Fig #1 – #3.

Fig #1 – Covid Stimulus Package – Source: Statista

Fig #2 – Monetary Bazooka – Source: Goldman, J.P. Morgan, Reuters, Ritvik Carvalho, Tommy Wilkes

Fig #3 – Fiscal Firepower – Source: Goldman, J.P. Morgan, Reuters, Ritvik Carvalho, Tommy Wilkes

Meanwhile, U.S. president Joe Biden has paved the way for his fiscal stimulus programme of $1.9 trillion dollars last March and just last month, has signed off a new infrastructure bill of $1.2 trillion dollars which is designed over an eight year period – it includes $109bn for roads and bridges, $66bn for railways, $49bn for public transport and $25bn for airports – that’s bullish for commodities!

The president wants to enact another, roughly $6tn spending package that would roll in his party’s priorities on climate change, education, paid leave and childcare benefits. And that’s just America! There are similar programmes all over the world, including Europe, China, Japan and elsewhere. Japan’s stimulus is so out of control, it now amounts to 56.09% per cent of its total GDP – unsustainable!

No wonder inflationary pressures are being stoked higher.

Inflationary Pressures Inevitable

The Federal Reserve has been watching how long-dated treasury yields have been trending strongly higher this year, widening the curve as it attempts to maintain its low-interest-rate policy. It had made several statements over the last months, saying inflationary pressures were ‘transitory’ in an attempt to halt the rise. The only other option would be to begin ‘yield curve control’ like the Bank of Japan – not desirable at all. The markets didn’t believe a word of this with bond fund managers increasing their short positioning as the latest Personal Consumption Expenditures (PCE) index, the key measure of the Fed’s inflation gauge surged higher.

US10yr treasury yields peaked in March at 1.774% and have been declining since to 1.245%, forcing bong managers to short-cover their positions amid a re-assessment of the inflation prospects. Ironically, in June’s Federal Reserve meeting, Chairman Jerome Powell announced a policy change, making a U-turn on inflation estimates, employment, the timing of a tapering of bond purchases and interest rate hikes. The Fed raised its headline inflation expectation to 3.4%, a full percentage point higher than the March ’21 projection. Therefore, it also shortened the time frame of interest rate hikes indicating two increases by end-2023. See graphic here:

Fig #4 – Stronger Inflation, lower unemployment – Source: Federal Reserves Summary of Economic Projections

Yes, inflationary pressures are inevitable and likely to continue trending higher right into the final peak of the inflation-pop cycle due in 2023/24. As a result, a shorter-term a pause also seems inevitable basis the Elliott Wave patterning across several key commodities like Copper, Crude oil, even Agricultural commodities and Foodstuffs.

Bullish Sentiment

Winding the clock back to the time when the coronavirus pandemic hit, commodities were under-invested by fund managers globally – see graphics here:

Fig #5 – Global Fund Manager Survey – Source: BofA

Fig #6 – Global Fund Manager Survey June 2021 – Source: BofA

In the March 2020 Global Fund Manager survey conducted by Bank of America, commodity exposure was shown to be at the lowest levels not seen since 2015 with energy in last position in the asset table. That certainly turned out to be a contrarian bullish signal. Fast-forward to today, and you’ll see commodity exposure has flipped 180 degrees and is now at the summit of the league table. From an Elliott Wave perspective, that’s another contrarian warning signal to expect a potential dip in prices over the next several months.

New Commodities Mid-Year 2021 Video – PART II/III

We’ve amassed over 109 commodity charts from our EW-Forecast database in this mid-year 2021 video. Each one provides a telling story into the way Elliott Wave price trends are developing as a ‘COMMODITY CORRECTION AHEAD’ with a ‘PAUSE WITHIN INFLATION-POP’ CYCLE’ development.

We invite you to take this next step in our financial journey with us. Video subscription details are below. Just follow the links and we’ll see you soon!

Most sincerely,

Peter Goodburn

Founder and Chief Elliott Wave Analyst

WaveTrack International

Commodities Video Part II

Contents: 109 charts

Time: 2 hours 42 mins.

• US PCE Inflation

• US Real Yield

• Food and Agriculture Index

• Lumber

• CRB-Cash index

• US Dollar index + Cycles

• Copper + Cycles

• Aluminium

• Lead

• Zinc

• Nickel

• Tin

• XME Metals & Mining Index

• BHP-Billiton

• Freeport McMoran

• Antofagasta

• Anglo American

• Kazakhmys Copper

• Glencore

• Rio Tinto

• Teck Resources

• Vale

• Gold + Cycles

• GDX Gold Miners Index

• Newmont Mining

• Amer Barrick Gold

• Agnico Eagle Mines

• AngloGold Ashanti

• Fresnillo Silver

• Silver + Cycles

• Silver/Copper Correlation

• XAU Gold/Silver Index

• Gold-Silver Ratio

• Gold/Platinum Spread

• Platinum

• Palladium

• Uranium

• Crude Oil + Cycles

• Brent Oil

• XLE Energy SPDR

• XOP Oil and Gas Index

• Natural Gas

How can you purchase the video?

1. Contact us @ services@wavetrack.com and ask for a PayPal payment link (please state if you like to purchase the Commodities Single video or the Triple Video?).

2. Ask for an individual credit card payment link (in case you do not with to pay via PayPal).

3. Simply pay online via VIMEO. CAVEAT! Vimeo does not allow PDF uploads – if you like the PDF report with the charts you can still contact us @ services@wavetrack.com with your purchase email from VIMEO and we will, of course, make it avaiable to you.

VIMEO – COMMODITIES VIDEO purchase here!

Here is the link to our STOCK INDICES Mid-Year Video Part I published on vimeo.

We will publish the Vimeo link here and/or you can follow us on VIMEO now to receive future updates.

*(additional VAT may be added depending on your country – currently US, Canada, Asia have no added VAT but most European countries do)

We’re sure you’ll reap the benefits – don’t forget to contact us with any Elliott Wave questions – Peter is always keen to hear you views, queries and comments.

Visit us @ www.wavetrack.com

We’re sure you’ll reap the benefits. Don’t forget to contact us with any Elliott Wave questions. Our EW-team is always keen to hear your views, queries, and comments.

Visit us @ www.wavetrack.com

Stock Indices Mid-Year Video Update

by WaveTrack International| June 24, 2021 | No Comments

Stock Indices Video | PART I/III

STOCK INDICES – ‘INFLATION-POP’ Goes Mainstream! Post-Pandemic Advance Set to Take a Pause within Final Stage of Secular-Bull Uptrend – Risk of -30-40% Correction in Benchmark Indices during next 6-Months – Inflationary Pressures Ease but Not Over – European Indices set for Significant Correction – EuroStoxx Banks Take a Hit – Small-Cap’s Suffer – Technology/FANGS+ Decline but Outperforming with Biotechnology – EM’s Correct as US$ Dollar Revives

Includes Updated SENTIMENT & ECONOMIC INDICATOR STUDIES

We’re pleased to announce the publication of WaveTrack’s Mid-Year 2021 video updates of medium-term ELLIOTT WAVE price-forecasts. Today’s release is PART I, STOCK INDEX VIDEO – Parts II & III will be published during July/August.

• PART I – STOCK INDICES

• PART II – COMMODITIES

• PART III – CURRENCIES & INTEREST RATES

Elliott Wave Stock Indices Forecast – Highlights

Stock Indices – Shorter-term U.S.

Upside rallies in the S&P 500, Dow, Russell 2000 and Nasdaq 100 indices from the post-pandemic March ’20 lows as intermediate wave (5) have so far unfolded into three wave a-b-c zig zag patterns. Risk of completing 1st waves within ending-type diagonals with 2nd wave corrections between -30% to max. -40% per cent over next 6-month period. Alternate bullish counts otherwise depict short-term correction of -10% per cent followed by higher-highs.

Stock Indices – Shorter-term Europe

The post-pandemic advance of March ’20 began a secondary A-B-C zig zag advance within the double pattern in upward progress from the financial-crisis lows of 2008-09. Wave A ended an initial advance into the July ’20 high – wave B is unfolding into an expanding flat with the high reached now. Final downswing beginning from current levels. Risk of -30% per cent decline over next 6-month period.

Stock Indices – Emerging Markets

MCSI Emerging Market index has traded higher from post-pandemic lows of March ’20 into an a-b-c zig zag. This is consistent within its 3rd wave double zig zag advance of the ending-type diagonal that began its uptrend in early-2016. An x wave correction is forecast lower by -30% per cent over next 6-month period.

Stock Indices – Global/Asia

Hang Seng is same pattern as MSCI EM index, trending higher as and ending-type diagonal but downside risks of correction during next several months. The Shanghai Composite underperforming but expected to outperform next year in 2022 once shorter-term correction has completed during next several months. Bovespa trending higher from post-pandemic lows as developing a-b-c zig zag. Corrective declines over next several months. Russia’s RTS vulnerable to a corrective dip but could outperform into year-end although dominant trend to the upside. India’s Sensex/Nifty 50 at risk of -30% to max. -40% per cent correction within post-pandemic uptrend. Singapore’s Straits Times underperforming but like China, expected to catch up next year. Taiwan SE index set for sizable correction within dominant uptrend. Australia’s All-Ord/ASX 200 set for a multi-month correction around -30% per cent before resuming to record highs afterwards. Nikkei 225 forecast lower over next several months by -35% per cent prior to resuming ending-type diagonal in advance from March ’20 lows.

Stock Indices Elliott Wave Forecast Review – H1 2021

The Annual 2021 report published last December (2020) forecast the continuing uptrend for global indices from the post-pandemic lows of March ’20. This was the final stage of the secular-bull uptrend that began from the financial-crisis lows of 2008-09.

Benchmark indices like the S&P 500 began 5th waves from the coronavirus lows with December’s report showing upside progress as a five wave expanding-impulse pattern. Shorter-term corrections were forecast as sentiment indicators reached levels of ‘extreme optimism’ but that never happened . Indices had already staged minor correction in September and were in the process of continuing more immediately higher. However, they never looked back and are still trading right now, at post-pandemic highs.

Sentiment Remains High

There’s been quite a few records broken in the process. Bank of America reports that the March ’20 recovery is the 3rd largest percentage rally on record – the other two were following major lows at the time of the Great Depression of 1932, in 1933 and 1936.

Their latest June ’21 Global Fund Manager Survey shows 76% per cent of investors believe the economy and the stock market is in an early-cycle ‘boom’ – see Fig #1. This reading is off-the-scale. By comparison, in previous peaks from the financial-crisis lows, readings were highest at 26-32% per cent. And even at the tops in early-2018!

Fig #1 – Global Fund Manager Survey – Source: Bank of America

Furthermore, that optimism is a straight-line advance from the post-pandemic low. However, it only went ‘exponential’ late last year when the northern-hemisphere summer holiday season ended. This is suggesting fund managers reassesses previous bearish call, turning very bullish from that time to present day.

The same survey reports net 75% per cent of fund managers expect a stronger economy which is just off a peak the previous month of 84% per cent. This high matches equivalent peaks in 1995, 2001, 2010 and 2014.

Now that’s really interesting!

Also, 68% per cent of fund managers don’t expect a recession until 2024 at the earliest – only 2% per cent expect a bear market in the next 6-months. Now that’s really interesting! The largest percentage of 47% believe a correction could unfold of less than <10% per cent and 6% per cent <20% per cent. That’s very skewed in optimism/complacency but only time will tell if this is a contrarian bear signal.

Elliott Wave Perspective

Certainly, from our Elliott Wave analysis, there’s a very high risk that markets will correct by more than the normal criteria of a -20% per cent for a ‘bear market’ but will instead decline between -30% to -40% per cent, depending on the index. If you want to understand the full story behind WaveTrack’s reasoning and analyis we invite you to watch our latest Stock Indices Video Part I/III.

New Stock Index Mid-Year 2021 Video – PART I/III

This MID-YEAR 2021 VIDEO UPDATE for STOCK INDICES is like nothing you’ve seen anywhere else in the world – it’s unique to WaveTrack International, how we foresee trends developing through the lens of Elliott Wave Principle (EWP) and how its forecasts correlate with Cycles, Sentiment extremes and Economic data trends.

We invite you to take this next step in our financial journey with us – video subscription details are below – just follow the links and we’ll see you soon!

Most sincerely,

Peter Goodburn

Founder and Chief Elliott Wave Analyst

WaveTrack International

Contents Stock Index Video Outlook 2021

Charts: 83 | Video: 2 hours 19 mins.

Read more «Stock Indices Mid-Year Video Update»

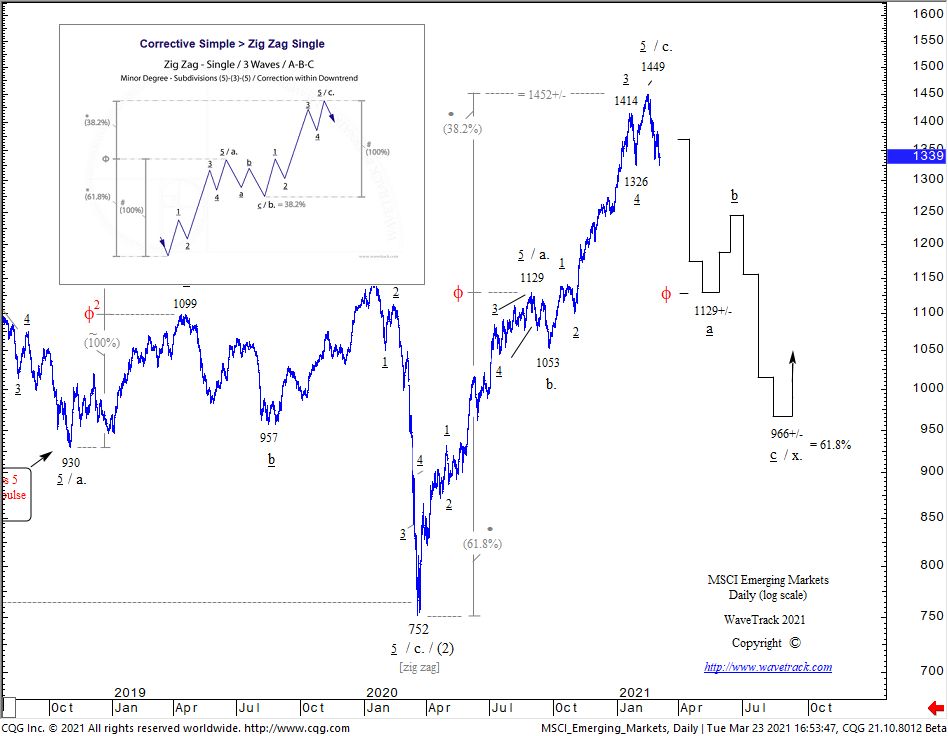

March ’20 Zig Zag Advances Completing 1st Wave Uptrends

by WaveTrack International| March 24, 2021 | No Comments

Advances from the March ’20 COVID-19 Pandemic Lows Unfolding into A-B-C (a-b-c) Zig Zags – Completes 1st Waves within Ending/Contracting-Diagonals as terminal high in Years 2023-24 – 2nd Wave Corrections Unfolding Now – Declines of -35% per cent Over Next 5-8 Months

Growth stocks

Growth stocks led the way during the early stages of the post-Coronavirus pandemic recovery of last year (2020). However, there’s since been a switch of outperformance in value stocks as growth got a bit stretched over the past couple of months. Rotation has also caused periods when large-caps lagged behind the outperforming small/mid-cap stocks/indices. Then there’s been a sudden underperformance in technology stocks/indices as long-dated treasury yields pushed strongly higher, making this industry less competitive relative to the broader market.

Critical Information

But amidst all of these uneven bumps, there’s emerged a defining Elliott Wave pattern development from the March ’20 COVID-19 lows. So many indices, large cap, mid-cap and small-cap together with several sectors alongside Emerging Markets/Asian indices have all unfolded into A-B-C zig zags. That’s really important. No, critical information because zig zags unfolding directionally higher following crash lows that formed last year can only be positioned in this case, within one type of larger Elliott Wave pattern – and that’s an ending-diagonal.

This month’s report examines how these A-B-C zig zags fit together into their larger degree ending-diagonal patterns across the major indices – see fig’s #1 & #2. But there’s a chilling outcome too. These zig zags are completing the 1st waves within developing five wave contracting-type diagonals which requires deep 2nd wave corrections. That could wipe out the current equity rally with declines of between -30% to -40% per cent over the next 5-8 month period.

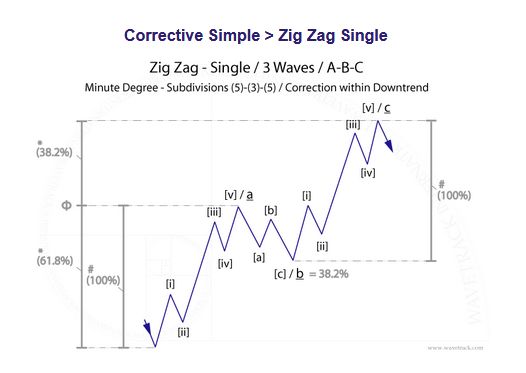

Fig #1 – Zig Zag Single

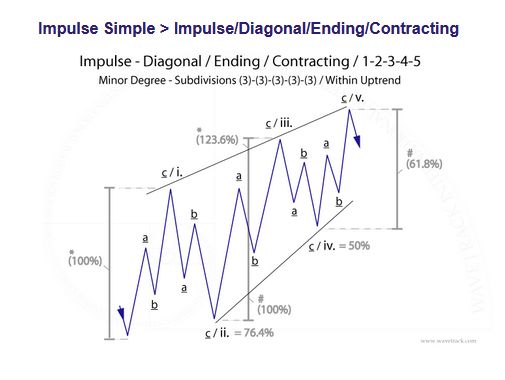

Fig #2 – Impulse Diagonal Ending Contracting by WaveTrack International

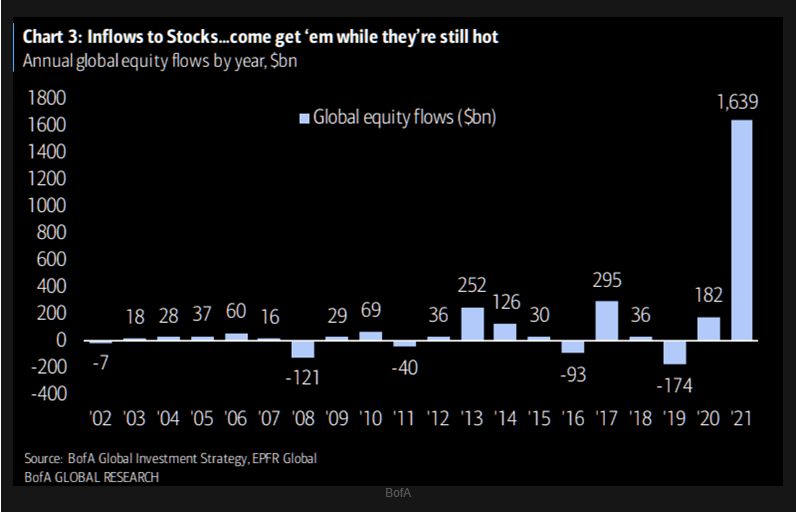

Such a decline could be triggered by any number of exogenous catalysts. For one thing, European countries are heading for a third-wave lockdown. The data backs-up the idea of a strong collapse in equities. Just look at the exponential gains in global equity flows so far this year which dwarfs anything every before – see fig #3. Exponential rises like this always turn into a parabolic curve, resulting in a deep downswing. That in itself could easily translate into a sharp downturn in evaporating fund allocation.

Fig #3 – Global Equity Flows – Source: Bank of America

Fund Manager Survey

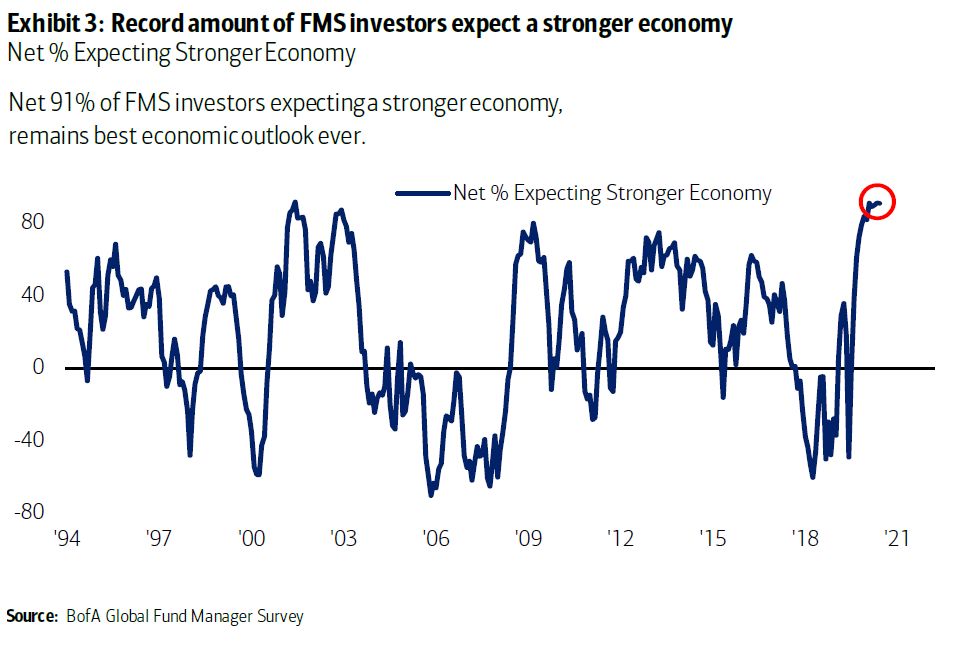

The latest Fund Manager Survey from Bank of America reveals that 91% per cent of FM’s expect a stronger economy for the remainder of this year. This is the highest figure EVER! – see fig #4. If that isn’t a bearish contrarian signal, then what is?

Fig #4 – Economic Outlook – Source: Bank of America

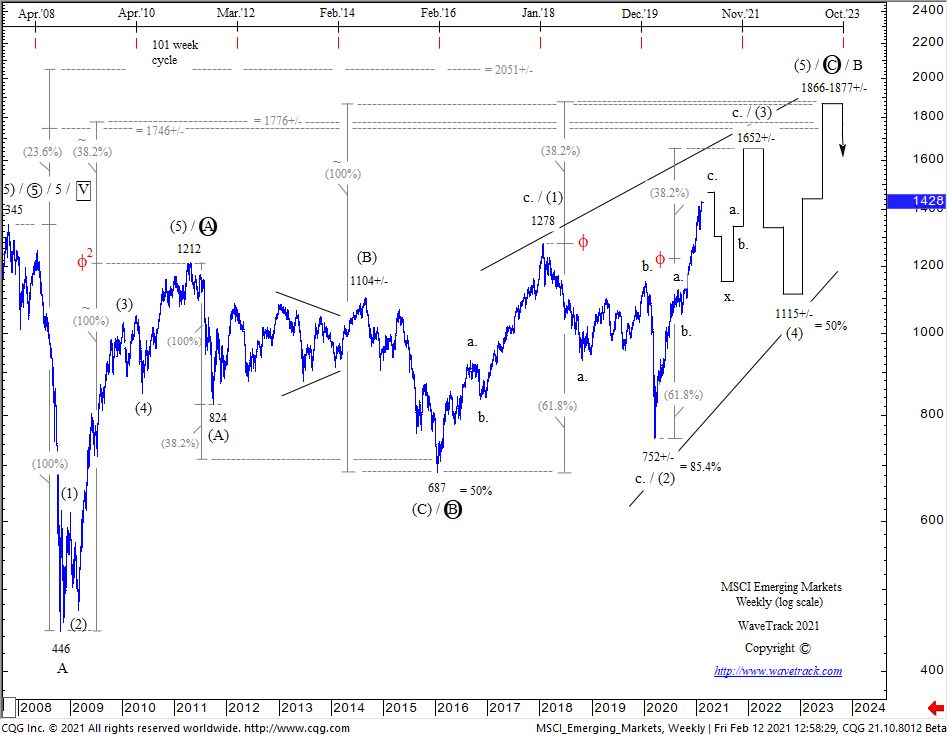

MSCI Emerging Markets

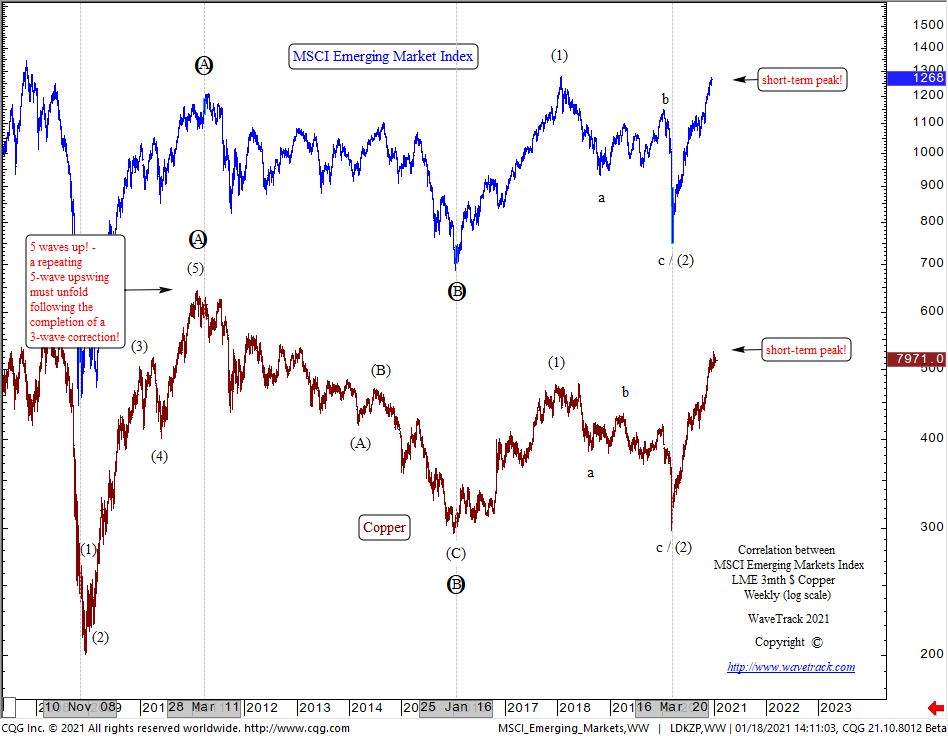

One of the benchmark illustrations of the Elliott Wave a-b-c zig zag advances from last year’s low is shown in the MSCI Emerging Market index – see fig #5. Note how wave a.’s high at 1129.00 x 61.8% equals the terminal high of wave c. at 1449.00. This ‘proofs’ its completion as the 1st wave within the larger degree ending/contracting-diagonal pattern. The final pattern of the secular-bull uptrend.

Fig #5 – MSCI Emerging Markets – Daily – WaveTrack International

A huge 2nd wave correction is about to get underway. Ordinarily, 2nd wave corrections within contracting-type diagonals retrace the 1st wave by fib. 76.4% per cent. But in our example, we’ve been more conservative showing the fib. 61.8% ret. level at 966.00+/-. But that’s still a decline of -33% per cent!

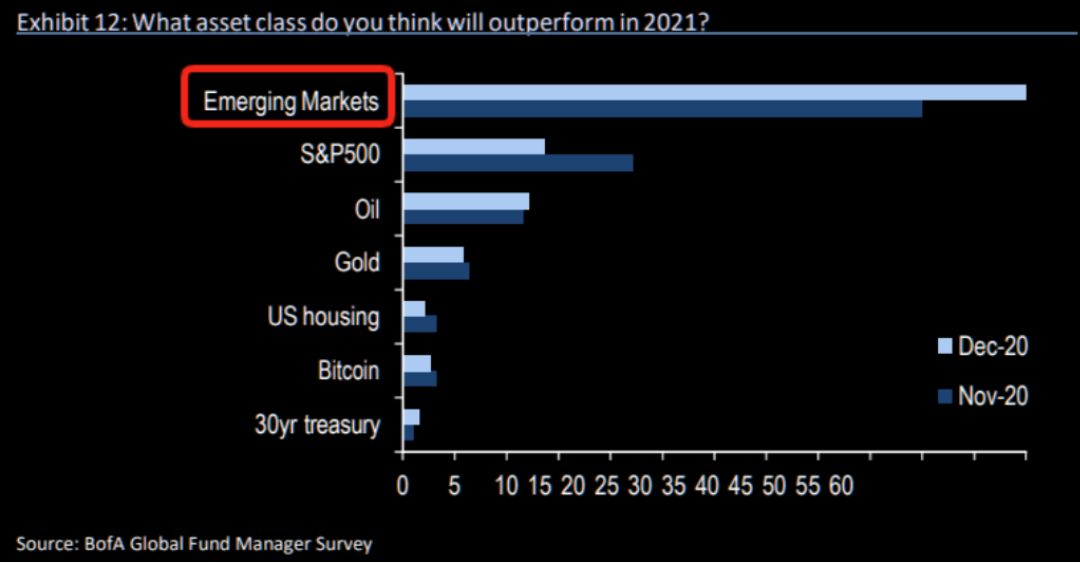

And recently, we’ve seen huge inflows into Emerging Markets. See Bank of America’s FMS survey results which show emerging markets are expected to be the No.1 outperformance asset class compared to the S&P 500, Crude Oil, Gold, U.S. Housing, Bitcoin and US30yr treasuries see fig #6.

Fig #6 – Asset Class Outperformance – Bank of America

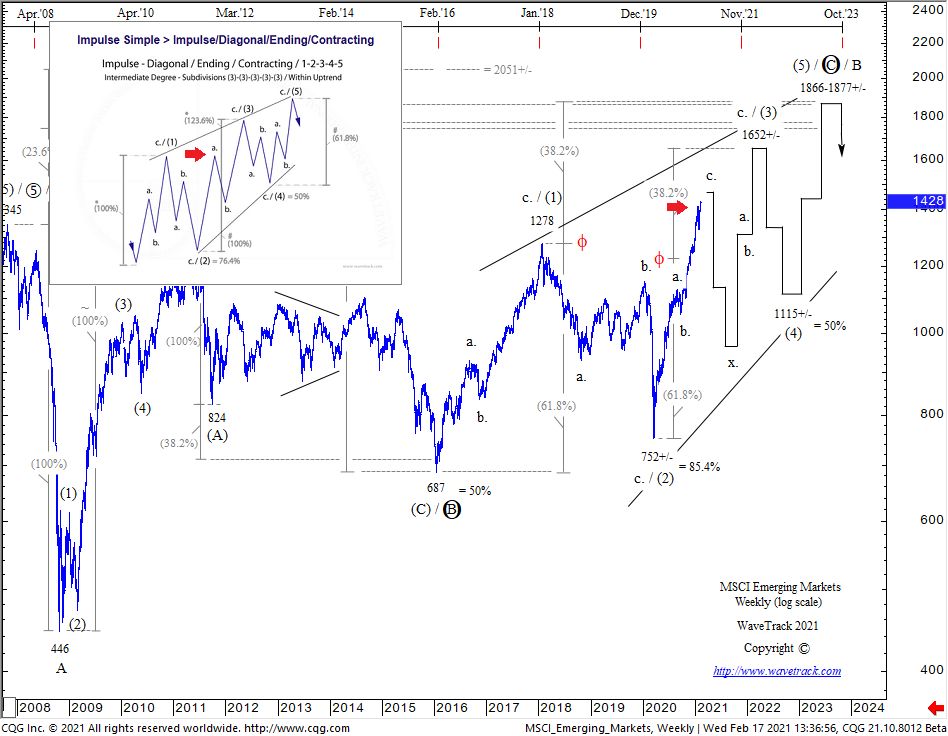

The MSCI EM’s diagonal pattern has been well documented in our Elliott Wave analysis for a number of years. Here’s an update of what it looks like today – see fig #7.

Fig #7 – MSCI Emerging Markets – Weekly by WaveTrack International

March ’20 Zig Zag Advances Completing 1st Wave Uptrends – read more in WaveTrack Elliott Wave Navigator report!

Currencies + Interest Rates Video Outlook 2021

by WaveTrack International| March 2, 2021 | No Comments

CURRENCIES and INTEREST RATES – PART III

US$ Dollar Index ends 9-Month Downtrend in January – Multi-Month Risk-Off/Safe-Haven Counter-Trend Rally Underway – Euro/US$ Hits Tops, Heading Lower in 5-6 Month Corrective Decline – Stlg/US$ Heading Lower – US$/Yen Higher with Yen Weakest in G10 – Commodity Currencies Set for 5-6 Month Corrective Declines – Asian ADXY Currencies begin Corrective Declines within Backdrop of Strengthening US$ Dollar – US10yr Treasury Yields Ending August ’20 Uptrend – Set for Multi-Month Correction – US10yr Breakeven Inflation TIPS ending Uptrend form March ’20 Lows – Reflation-Trade Unwinds over next 5-6 Months – DE10yr Yields Trending Higher but Beginning Corrective Downswing

INCLUDES ANALYSIS ON MAJOR US$ DOLLAR PAIRS/CROSSES – ASIAN/EM CURRENCIES – MEDIUM-TERM CYCLES – LONG-DATED YIELDS US/EUROPE/JAPAN + SPREADS

We’re pleased to announce the publication of WaveTrack’s annual 2021 trilogy video series of medium-term ELLIOTT WAVE price-forecasts. Today’s release is PART III, CURRENCIES & INTEREST RATES – Parts I & II were released during the last month – please contact us for information.

• PART I – STOCK INDICES – OUT NOW!

• PART II – COMMODITIES – OUT NOW!

• PART III – CURRENCIES & INTEREST RATES

CURRENCIES REVIEW – Highlights from Mid-Year 2020

• The US$ dollar index has resumed its 7.8-year downward cycle from March’s COVID-19 price-spike high of 102.99. Over the next several years, the dollar is forecast significantly lower as primary wave 3 gains downside momentum – forecasts towards 56.00+/-

• Shorter-term, the US$ dollar index is approaching downside targets towards 91.00+/- for the completion of an initial five wave impulse pattern from March’s 102.99 high. This combined with an extreme ‘oversold’ reading indicates a dollar counter-trend upswing will unfold for the next 2-3 months

The actual low in the US$ dollar index was 89.21, traded last January ’21. Since then, the dollar has begun a 5-6 month counter-trend rally which is forecast unfolding into a typical [a]-b]-[c] zig zag correction heading for the fib. 50% retracement area around 95.85/-. This is confirming a switch from the existing ‘Risk-On’ ‘Reflationary-Trade’ strategies to ‘Risk-Off’ ‘Reflationary-Trade Unwinding’ within a Safe-Haven period lasting into the end of Q3 2021.

Currencies – Key Drivers/Events for 2021

The US$ dollar has been declining for almost a year now, having ended a 2-year counter-trend rally peak into the March 20 COVID-19 pandemic peak of 102.99. At the core of this decline is the sheer amount of monetary and fiscal stimulus central banks and governments are willing to use to combat the effects of economic fallout due to the global coronavirus pandemic. The Federal Reserve and the new U.S. administration of Joe Biden are a good example – National Debt has surged higher to $27.86 trillion dollars – see fig #1.

Fig #1 – US National Dept – WaveTrack International – Currencies and Interest Rates Video Outlook 2021

This chart courtesy of WolfStreet.com shows exactly what’s happened since March ’20, the cut-off line at the height of the coronavirus pandemic. The rise in debt has gone exponential since then, rising by $4.55 trillion in just under 12 months. That will undoubtedly cause rising inflationary pressures going forward, weakening the US$ dollar in the process.

EW-Forecasts for 2021

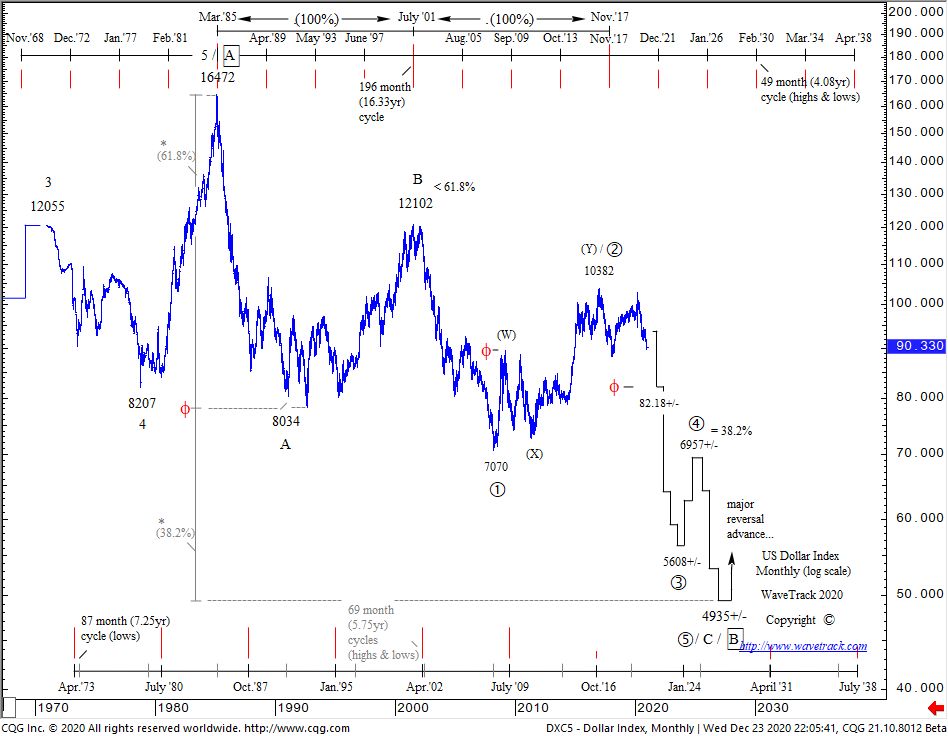

If you’ve tuned-in to our annual reports before, you’ll already know that the US$ dollar index is engaged in a 7.8-year cycle downtrend that began from the Jan.’17 high of 103.82. This is labelled as primary wave 3 within an Elliott Wave impulse downtrend that began from the July ’01 high of 121.02. You can probably imagine this means the dollar is set to decline rapidly over the next several years.

Fig #2 – 2021 Asset Performance – Source: Bank of America

So far this year, over the past 8-weeks, the Asset Performance league table shows the US$ dollar index holding onto recent lows traded in early-January above its low of 89.21 – see fig #2. Gold features as the worst performer although that’s more to do with the fact that long-dated interest rates have been trending strongly higher. Otherwise, the star performers are commodities, the CRB index, Crude/Brent oil, Copper and to some extent, Emerging Markets. These have all continued advancing strongly in accordance to the existing ‘Risk-On’ ‘Reflationary-Trade’ strategies. But that’s about to change!

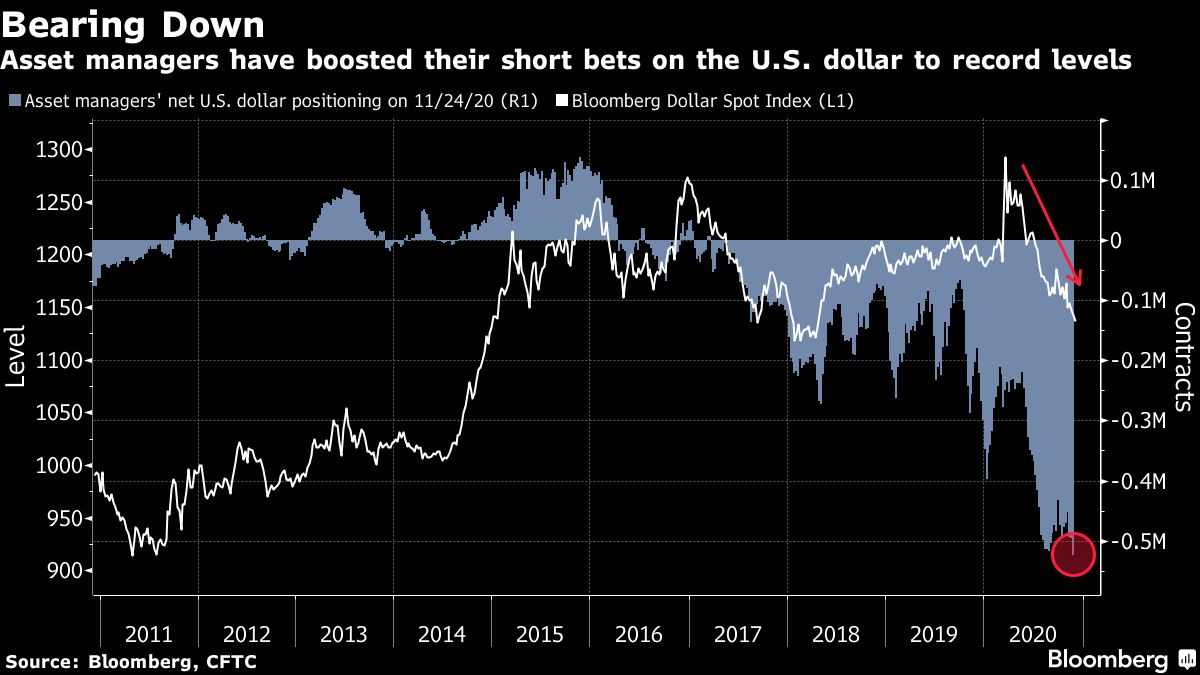

The Next 5-6 Months

The US$ dollar remains very oversold, in fact, asset managers have increased their short-positioning to record levels in early-January – see fig #3. The numbers show in excess of -500,000 short contracts which was nowhere near levels seen back in 2011 when the dollar was actually trading a lot lower.

Fig #3 – USD Short Positioning at the Extreme – Source: Bloomberg

Furthermore, in its latest Fund Manager Survey, Bank of America/Merrill Lynch asked its fund manager clients what they considered the most crowded trades. In 3rd position was a Short-Dollar positioning with only Long Technology and Bitcoin ahead of it. That’s really something! See fig #4.

Fig #4 – USD Short Positioning – Source: Bank of America

We know that such statistics can be misleading when it comes to timing imbalances that eventually lead to directional change, but sentiment data like this can be used in conjunction with Elliott Wave analysis which we can confirm shows that dollar oversold condition is about to change with significant corrective rallies already underway. The US$ dollar index is forecast up to 95.85+/- over the next 5-6 months, maybe even higher.

Fig #5 – British Pound Year-to-Date Performance – Source: Reuters

Ahead of this change, the best performing currency so far this year has been Stlg/US$ – see fig #5. That’s surprising when you consider this post-Brexit, but there you are! The Norwegian Krona is next in the league table, but that’s not surprising given the strength in Crude/Brent oil prices. In fact, all the commodity currencies in the G10- basket have done pretty well, especially since the March ’20 COVID-19 lows.

Latest Annual Report

The main theme for Currencies underlines the long-term downtrend of the US$ dollar within the backdrop of rising inflationary pressures but a 5-6 month period where this dissipates, where the dollar begins a counter-trend rally which means all the other dollar currency pairs with the G10 will decline into corrections during the same period.

Emerging Market currencies will decline over the next 5-6 months, as will nearly all Asian currencies we track within the ADXY basket. This report updates many currency crosses, totalling 98 charts!

Interest Rates

We know that long-dated interest rates are on the rise, capturing the headlines over recent weeks. This has caught the bond markets by surprise because of the commitment from the Federal Reserve and other central banks around the world including the ECB, Bank of Japan and Bank of China in maintaining unlimited monetary stimulus through bond purchases. But that hasn’t prevented the long-dated interest rate maturities from rising dramatically since January. The main reason is that investors are worried that reflationary pressures are exerting themselves with no end in sight.

The ‘Real Yield’ as measured in 30yr treasuries is approaching zero 0.00% per cent having spent most of the time in negative since the COVID-19 pandemic broke last year – see fig #6. It was last year’s real yield plunge which sent cash flooding into stock markets. While expensive, they looked like a good deal compared with real yields of minus -1%. But fiscal stimulus and prospects of economic reopening have lifted real 30-year Treasury yields to eight-month highs, just 11 basis points shy of 0% and that’s what’s getting investors agitated. Could yields continue to exponentially rise? We think not!

Fig #6 – Real Yield – Source: US Department of the Treasury

Whilst the long-term trends show a new 30+ year uptrend cycle for global interest rates, including treasury yields began from before last year’s COVID-19 pandemic lows, it is due to take a breather over the next 5-6 months. The uptrend in the US10yr treasury yield has begun from last year’s historical low of 0.378% unfolding into a typical Elliott Wave 1-2-1 formation, a preamble to a strong multi-year uptrend. But the August ’20 advance from the secondary low of 0.500% has just completed a five wave impulse pattern into the late-February high of 1.554%. It’s necessary for a counter-trend 2nd wave downswing to now unfold. This suggests a temporary unwinding of the ‘Reflation-Trade’.

In Bank of America/ML’s GFM survey, the expectations of a steeper dollar yield curve are at levels above those during the Lehman bankruptcy crisis of 2008! See fig #7. That reflects just how bearish bond holders are, and conversely, why US10yr yields are too high at the moment. A contraction in the yield curve would almost certainly translate into a correction in benchmark US10yr treasury yields for the remainder of this year.

Fig #7 – Steeper Yield Curve – Source: Bank of America

This latest annual report also examines the benchmark German DE10yr yield alongside the US10yr-DE10yr spread and Italian and Japanese yields/trends.

New Currencies & Interest Rates 2021 Video – PART III/III

We’ve amassed over 130 charts (a new record!!) from our EW-Forecast database in this year’s Currencies & Interest Rates 2021 video. Each one provides a telling story into the way Elliott Wave price trends are developing in this next INFLATION-POP’ phase of cycle development. We’re taking a look at some very specific patterns that span the entire 15.6-year US$ dollar cycle, explaining its current location and why inflation will trigger huge US$ dollar declines but simultaneously appreciating major Emerging Market and Asian Currencies.

We’re updating some amazing Elliott Wave forecasts for U.S. interest rates, US10yr, US10yr, US05yr and even US02yr together with a schematic look at several spread relationships with European rates not forgetting upside targets for the US10yr Inflation Tips – it’s a must-see!

We invite you to take this next step in our financial journey with us – video subscription details are below – just follow the links and we’ll see you soon!

Most sincerely,

Peter Goodburn

Founder and Chief Elliott Wave Analyst

WaveTrack International

What you get!

Contents: 130 charts | VIDEO DURATION: 2 hours 54 mins.

The contents of this CURRENCY & INTEREST RATES VIDEO include Elliott Wave analysis for:

Currencies (100 charts):

• US$ Index + Cycles

• Euro/US$ + Cycles

• Stlg/US$

• US$/Yen

• US$/CHF

• US$/NOK

• US$/SEK

• AUD/US$

• US$/CAD

• NZD/US$

• Euro/Stlg

• Euro/CHF

• Euro/NOK

• Euro/Yen

• Euro/AUD

• Euro/CNY

• Stlg/YEN

• Stlg/CHF

• Stlg/NOK

• Stlg/ZAR

• Stlg/AUD

• AUD/NOK

• CAD/NOK

• AUD/CAD

• AUD/NZD

• Asian ADXY

• US$/Renminbi

• US$/KRW

• US$/SGD

• US$/INR

• US$/TWD

• USD/THB

• US$/MYR

• US$/IDR

• US$/PHP

• USD/BRL

• USD/RUB

• US$/ZAR

• US$/MXN

• US$/TRY

• US$/PLZ

• Bitcoin

Interest Rates (30 charts):

• US30yr Yield + Cycles

• US10yr Yield + Cycles

• US5yr Yield

• US2yr Yield

• US2yr-10yr Yield Spread

• US10yr-30yr Yield Spread

• 3mth EuroDollar-US10yr Yield Spread

• Comparison US10-DE10yr vs S&P 500

• US10yr TIPS Break Even Inflation Rate

• US10-DE10yr Yield Spread

• DE10yr Yield

• ITY10yr Yield

• JPY10yr Yield

>How to buy the Currencies + Interest Rates Video Outlook 2021

Simply contact us @ services@wavetrack.com to buy the CURRENCIES + INTEREST RATES Video Outlook 2021 for USD 48.00 (+ VAT where applicable) or alternatively our Triple Video Offer for USD 96.00 (+ VAT where applicable) – Review the content of WaveTrack Stock Indices Video PART I here and the Commodities Video PART II here.

*(additional VAT may be added depending on your country – currently US, Canada, Asia have no added VAT but most European countries do)

We’re sure you’ll reap the benefits – don’t forget to contact us with any Elliott Wave questions – Peter is always keen to hear you views, queries and comments.

Visit us @ www.wavetrack.com

Ending-Diagonal Patterns as Last Sequence within Secular-Bull?

by WaveTrack International| February 17, 2021 | No Comments

Ending-Diagonal Patterns as Last Sequence within Secular-Bull / Inflation-Pop Cycle Uptrends

Fig #1 – Russell 2000 – Weekly by WaveTrack International

Fig #2 – S&P 400 Mid-Cap Index – Weekly by WaveTrack International

Fig #3 – Value Line Arithmetic Index – Weekly by WaveTrack International

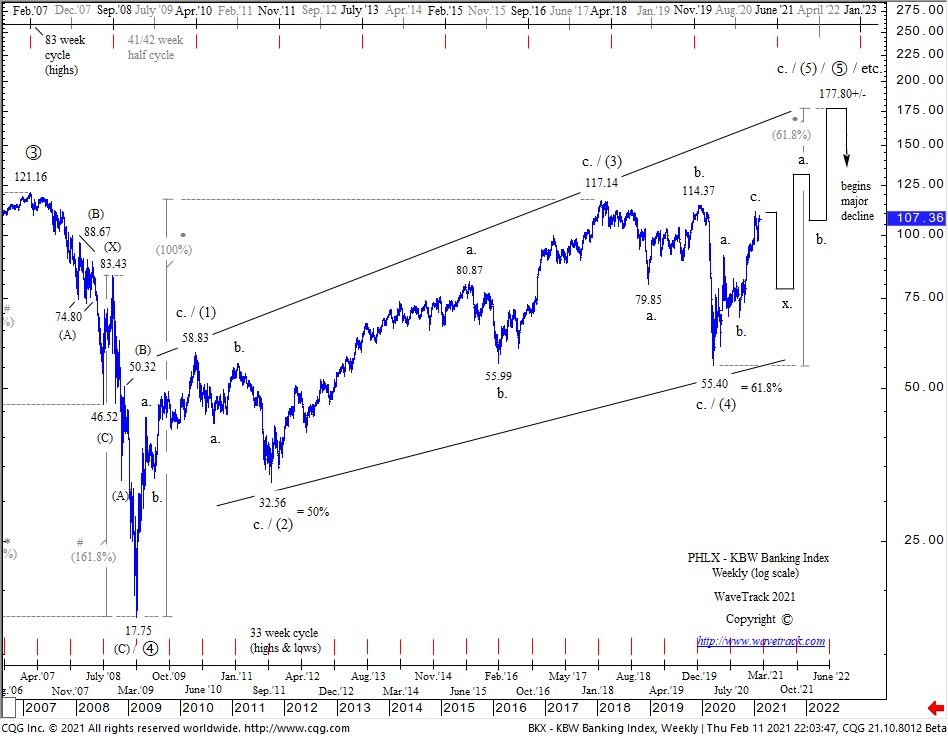

Fig #4 – KBW Banking Index – Weekly by WaveTrack International

Fig #5 – MSCI Emerging Markets – Weekly by WaveTrack International

Fig #6 – Hang Seng – Weekly by WaveTrack International

Fig #7 – S&P Nifty 50 – Weekly by WaveTrack International

Fig #8 – Nikkei 225 Index – Weekly by WaveTrack International more deteails published in the Elliott Wave-Compass Report www.wavetrack.com

Ending-Diagonal Patterns as Last Sequence within Secular-Bull/Inflation-Pop Cycle Uptrends – read more in today’s Elliott Wave Compass report!

Tags: Ending-Diagonal Elliott Wave Pattern

Zig Zag Rallies from March ’20 COVID-19 Lows

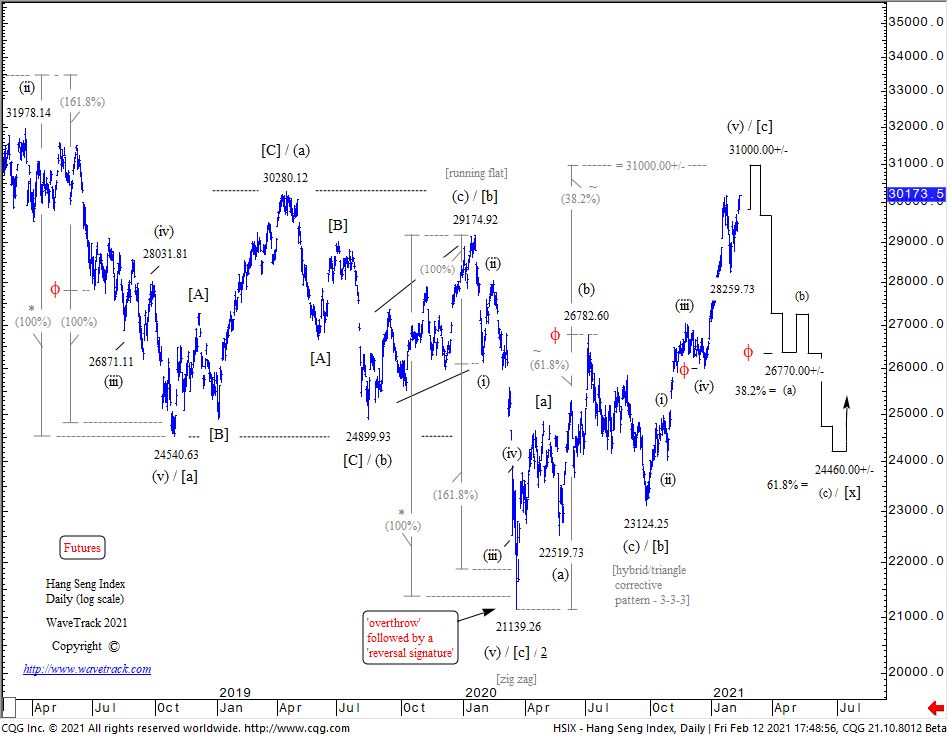

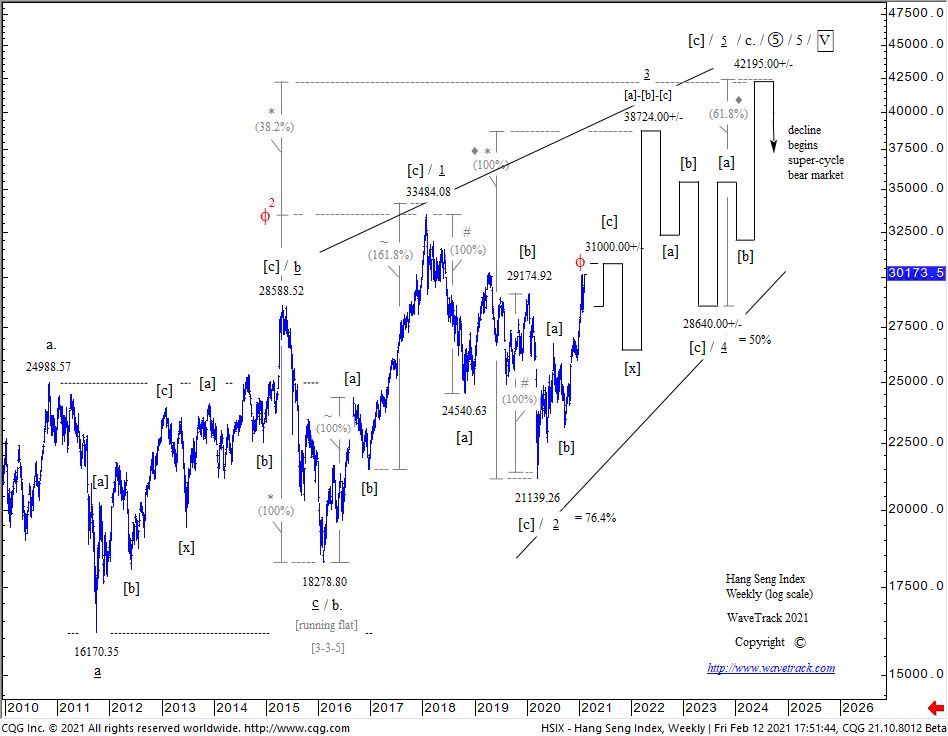

by WaveTrack International| February 12, 2021 | No Comments

MSCI Emerging Market Index – Hang Seng – KBW Banking Index

Fig #1 – MSCI Emerging Market – Daily

Fig #2 – MSCI Emerging Markets – Weekly

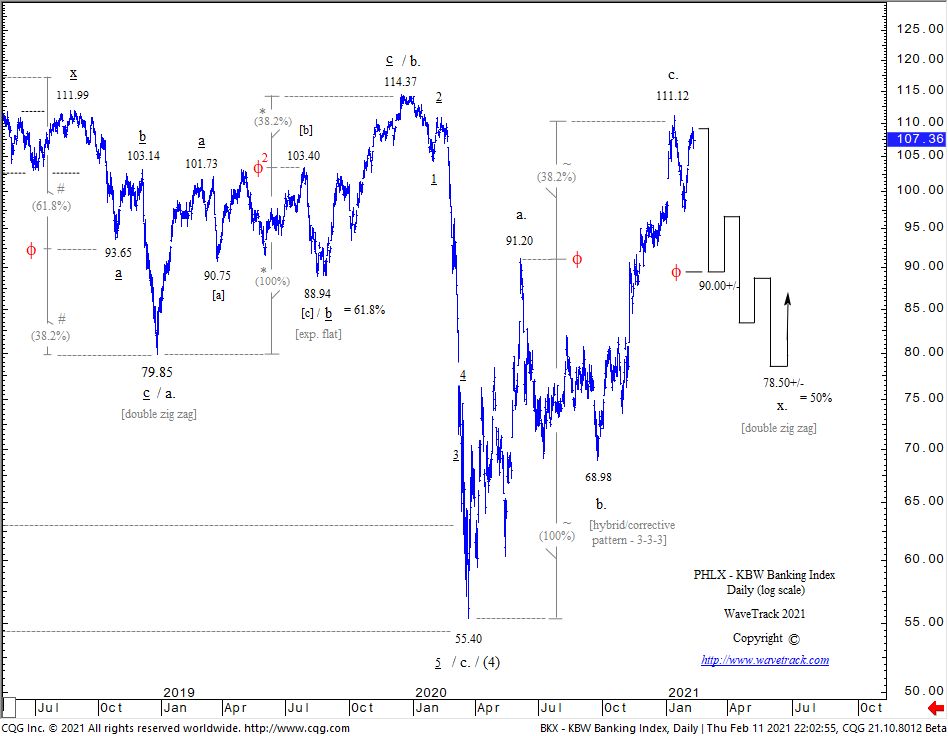

Fig #3 – PHLX – KBW Banking Index – Daily

Fig #4 – PHLX – KBW Banking Index – Weekly

Fig #5 – Hang Seng Index – Daily by WaveTrack International

Fig #6 – Hang Seng – Weekly by WaveTrack International

Zig Zag Rallies from March ’20 COVID-19 Lows – read more in today’s Elliott Wave Compass report!

COMMODITY Video Outlook 2021 | Part II

by WaveTrack International| January 22, 2021 | No Comments

‘FINAL STAGE of the COMMODITY ‘INFLATION-POP UPTREND’

THIS REPORT INCLUDES ANALYSIS ON MEDIUM-TERM CYCLES & EQUITY MINERS

We’re pleased to announce the publication of WaveTrack’s annual 2021 video updates of medium-term ELLIOTT WAVE price-forecasts. Today’s release is PART II, COMMODITY VIDEO OUTLOOK 2021 – Part I was released last month and Part III will be published in early-February.

• PART I – STOCK INDICES – out now!

• PART II – COMMODITIES – out now!

• PART III – CURRENCIES & INTEREST RATES – coming soon!

Commodity Elliott Wave Forecasts 2021 – Summary

• The Commodity Super-Cycle began from the Great Depression lows of year-1932, typically unfolding over the next 76-year period into an Elliott Wave impulse pattern ending in year-2008. Since then, a two-decade long corrective downswing has begun a new deflationary era but with pockets of rising inflationary pressures.

• Rising inflationary pressures began after the financial-crisis of 2007-09. The next stage resumed in early 2016, took a pause in 2018-2020 and is now set to surge higher through 2023/24 – this is the final stage of the ‘Inflation-Pop’ uptrend/cycle.

• Commodities have undergone extreme sell-offs during the COVID-19 panic that lasted through the first-quarter of 2020. Last January’s report cited a ‘Q1 Sell-Off’ prior to a major recovery. And that’s exactly what’s happened! All commodity sectors were hit hard, Base Metals, Precious Metals & Energy but especially Crude/Brent oil. Since then, major recoveries have begun and these are seen lasting into the next cycle peaks due in 2023/24.

• The US$ dollar resumed its 7.8-year cycle downtrend in March ‘20. An Elliott Wave 3rd-of-3rd wave is set to accelerate lower over the next several years. This becomes one of the main drivers that pushes commodity prices sharply higher.

• Shorter-term, commodity price advances from the March ’20 COVID-19 pandemic lows are approaching interim peaks having unfolded higher into five wave impulse patterns. A multi-month corrective downswing is forecast through Q1 and part of Q2 ’21 coinciding with a counter-trend rally/advance in the US$ dollar – begins a risk-off period.

• Base Metals Copper, Aluminum, Lead and Zinc have all trended higher from their March ’20 COVID-19 pandemic lows into five wave impulse patterns that are only now approaching completion. A multi-month correction is set to begin, pulling prices lower for several months.

• Precious Metals Gold and Silver both ended 3rd wave peaks last August ’20 and have since been engaged in multi-month counter-trend 4th wave declines. The price-extremities are lower for gold but already reached for silver. Gold is forecast lower into July ’21 basis its composite cycle. Platinum is expected to outperform gold but is also engaged in a counter-trend decline from its Jan.’21 high.

• Energy Price advances from the April ’20 lows for both Crude/Brent oil have unfolded into three wave A-B-C zig zag formations, ending right now, into January ’21 highs. A multi-month risk-off decline is forecast through to mid-year where prices retrace fib. 38.2% to max. 50% of the preceding advance from the COVID-19 pandemic lows. Thereafter, surging higher again through to 2023-24 as the final stage of the ‘Inflation-Pop’ uptrend/cycle.

Risk-Off Correction Beginning Q1 – ‘Inflation-Pop’ Uptrends Resume Q3

Commodities have surged higher over the past 10-month period having collapsed into important lows last year during the March ’20 COVID-19 pandemic. These advances represent the ‘Final Stage of the Inflation-Pop Uptrend’ which is poised to accelerate commodity prices significantly higher over the next several years.

The Elliott Wave pattern rhythm of Commodity price rises from the ‘Inflation-Pop’ lows of 2007-09. This is archetypically different to the same advance unfolding in global stock indices from the financial-crisis lows – see fig #1. This is often misunderstood. Yet, it can be explained from observing the historical long-term trends of both, from the Great Depression lows of 1932.

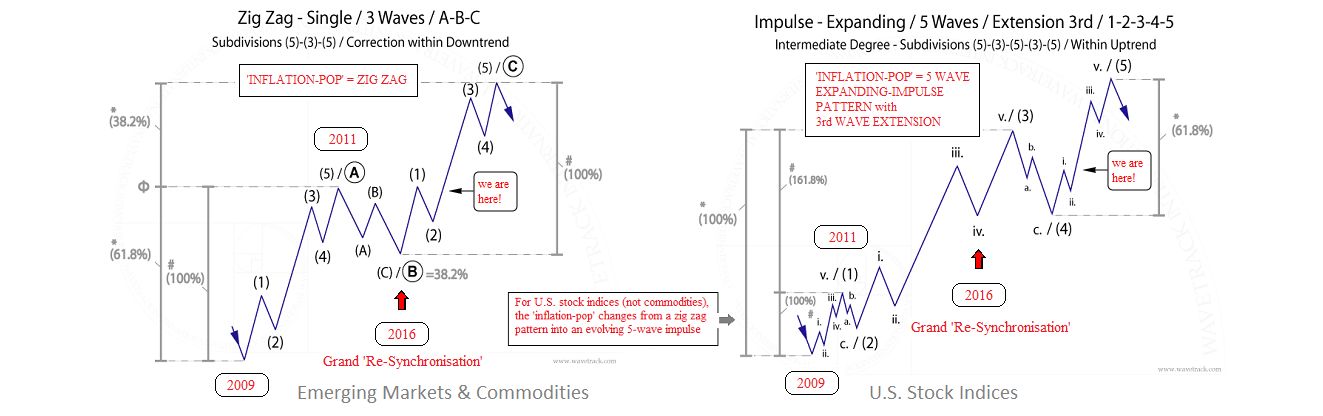

Fig # 1 – Inflation Pop vs. 5 Wave Impulse Pattern

When these two asset classes began long-term uptrends from 1932, they both unfolded into cycle degree five wave impulse patterns. This commodity super-cycle actually ended its five wave structure in year-2008. However, U.S. stock markets have continued their equivalent pattern higher. The financial-crisis sell-off into the late-2008/early-2009 lows triggered the beginning of a multi-decennial A-B-C expanding flat pattern for commodities, ending cycle wave A but this low was simply a 4th wave correction for stock markets. The next advance for commodities represents cycle wave B, itself a primary degree A-B-C zig zag (see tutorial chart) pattern destined for new record highs. Meanwhile, the same period for U.S. stock indices began a 5th wave which must ultimately subdivide into a five wave impulse pattern. Most importantly, these two differing Elliott Wave patterns have been unfolding ever since.

Positive Correlation

Their positive-correlation remained in sync during the initial ‘Inflation-Pop’ advance from 2009 to 2011 but then it broke-down for five years. It was necessary because commodity prices had to begin a corrective downswing as primary wave B. But for U.S. stock indices, they were simultaneously engaged in accelerative third-wave advances within the larger 5th wave uptrend. This disparity was eventually reconciled when both declined into formative lows in late-2015/early-2016. At the time, we described this event as the grand ‘Re-Synchronisation’.

Final Stage of the Inflation-Pop Uptrend

Since then, commodity prices, especially Base Metals and their corresponding Mining Stocks have traded higher in huge multiple gains. And those uptrends are still engaged to the upside. There was another sub-sector disparity which has subsequently been realigned when Energy contracts like Crude Oil and Brent oil collapsed last year, into the April ’20 COVID-19 lows. But advances in both underlying Base Metals and Energy contracts have since entered the Final Stage of the Inflation-Pop Uptrend’ which is poised to accelerate prices significantly higher over the next several years. So what is triggering these events?

Monetary & Fiscal Stimulus

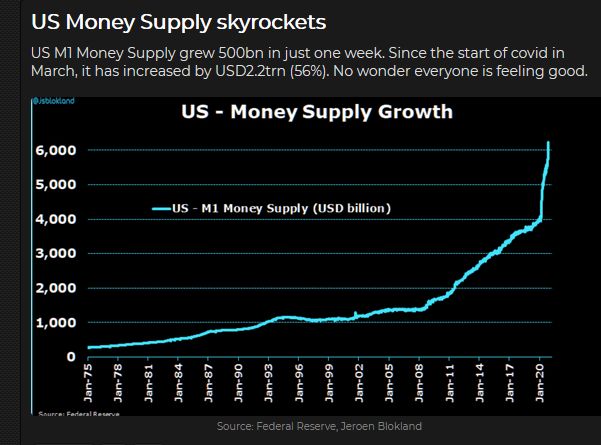

Central banks have responded to the COVID-19 pandemic by significantly increase money supply – see fig #2.

Fig #2 – Money Supply Skyrockets – Souce: Federal Reserve

The U.S. Federal Reserve alone has increased M1 money supply so much the figures saw an increase of $2.2 trillion dollars, a sudden jolt to existing debt representing a 56% per cent increase. With so much money sloshing around, its no wonder that asset prices are rising across-the-board.

Commodity Outlook 2021 and the US$ Dollar Outlook

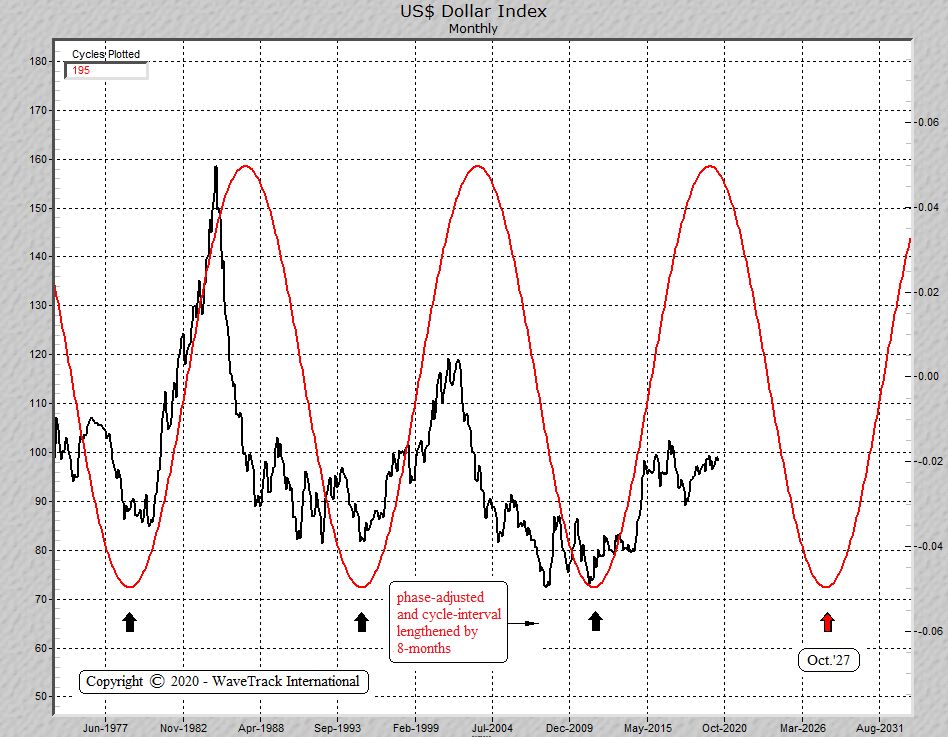

One contributor that’s expected to drive asset values significantly higher over the next few years is a weakening US$ dollar – see fig #3. There’s a distinct 15.6-year cycle recurrence for the US$ dollar index which has signalled the various peaks and troughs over the past several decades. In this updated cycle, the length of the interval has been increased to 16.25 years in order to align the cycle-troughs of the late-1970’s, mid-1990’s, early-2010’s into the next major lows of 2027.

Fig #3 – US Dollar Index – Monthly Cycle by WaveTrack International

Such US$ dollar declines are shown unfolding as the final sequence of the dollar index’s cycle degree A-B-C downswing that began from all-time-highs of 164.72 that peaked back in February 1985 – see fig #4. Looking ahead over the next several years, we expect the dollar to decline rapidly. To be exact, around -45% per cent fuelling the final stage of the commodity inflation-pop. Downside targets are towards 56.08+/- and ultimately 49.34+/-.

Fig #4 – US Dollar Index – Monthly Elliott Wave Forecast by WaveTrack International

Risk-Off Correction Beginning Q1 2021

Before commodity prices resume their inflation-pop uptrend, there’s going to be a risk-off correction beginning Q1 ’21 lasting though to mid-year. What triggers this? Most probably, a US$ dollar counter-trend rally!

Fig #5 – USD Short Positioning – Source: Bloomberg

Asset managers have a net U.S. dollar positioning at extreme record lows – see fig #5. That alone suggests the dollar index will soon begin a multi-month counter-trend rally. But does this corroborate with Elliott Wave and cycle analysis? Yes, the daily composite cycle is forming an important low right now, into January 2021 – see fig #6. Moreover, from an EW perspective, the index’s decline from the March ’20 COVID-19 peak of 102.99 is ending a five wave impulse pattern at January’s low of 89.21. This confirms a dollar risk-off/safe-haven phase has begun, lasting through to mid-year, maybe longer? That would certainly cause commodity prices to undergo significant corrective declines.

Fig #6 – US Dollar Index – Daily – Cycle by WaveTrack International

We can’t always know what fundamentals trigger such events, but a good guess is another downturn in global economic activity as COVID-19 second-phase lockdowns continue for another few months.

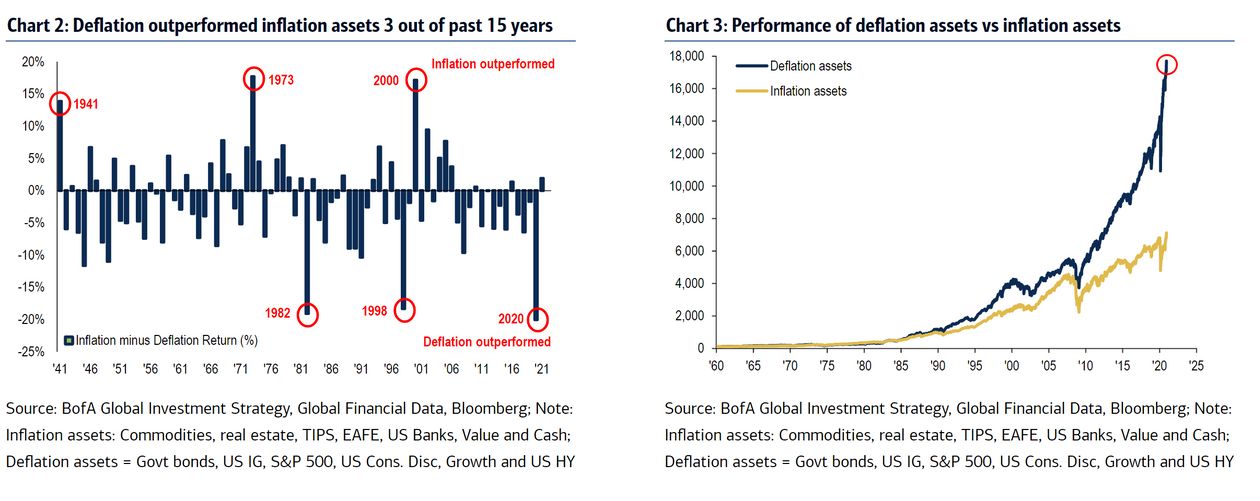

Commodity Deflation/Inflation

Another indication of risk-off during the next several months comes from interpreting Bank of America’s deflation/inflation data as a ‘contrarian’ indicator – see fig #7. Bank of America lists inflation assets as commodities, real estate, Treasury inflation-protected securities (TIPS), U.S. banks and value stocks. Deflation assets include government bonds, corporate bonds, the S&P 500, and growth stocks.

Fig #7 – Deflation Outperformed Inflation Assets – Source: Bank of America

They report that inflation assets are outperforming deflation assets by the most since 2006 and that’s a direct result of large asset managers believing the central bank and fiscal stimulus narrative and consequently buying undervalued assets. This really began last August/September ’20 – up until then, asset managers were expecting a double-dip recession but they quickly changed tack afterwards and have since binged on buying these inflationary assets, particularly commodities and emerging markets – see fig #8. Just last week saw the second-largest inflow to energy stocks, the third-largest inflow to Treasury inflation-protected securities, sixth-largest inflow to emerging markets, and the largest inflows to bank loans in nearly four years, according to the Bank of America data. Municipal bonds, which are exempt from federal and most state taxes, saw record inflows.

Fig #8 – MSCI Emerging Markets Index vs. Copper – Correlation Study by WaveTrack International

And to a point that now looks like an extreme – from a contrarian standpoint, a ripe environment for a correction to begin in 2021!!

Commodities – Copper, Gold & Energy

Copper prices have advanced from their March ’20 COVID-19 lows to begin the final stage of the ‘Inflation-Pop’ uptrend/cycle. Elliott Wave analysis forecasts new record highs over the next several years leading into the expected peak around 2023-24. But shorter-term, a correction lasting for the next several months is about to get underway in response to finishing a five wave impulse uptrend.

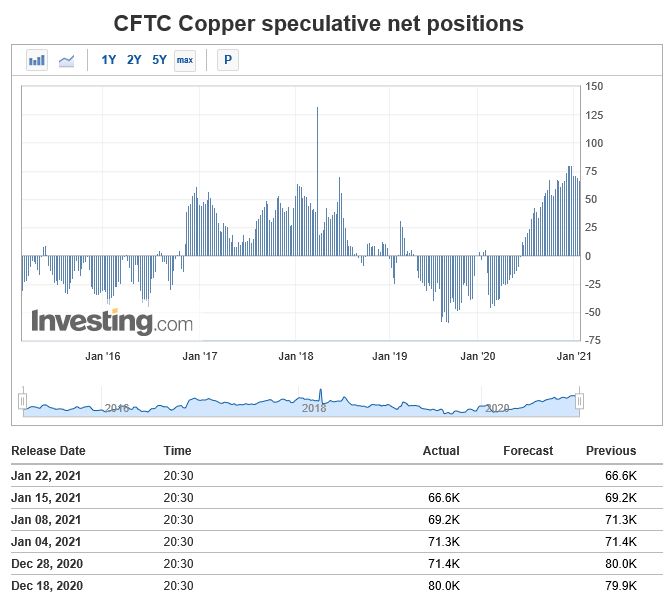

Fig #9 – CFTC Copper Speculative Net Positions – Source: Investing.com

The latest CFTC data shows frothy net speculative long positioning at 66,600 contracts, historically high – see fig #9. That’s down from 80,000 late-December but still well above 5-year highs, an early-warning that prices are a little top-heavy.

US 10yr Tips

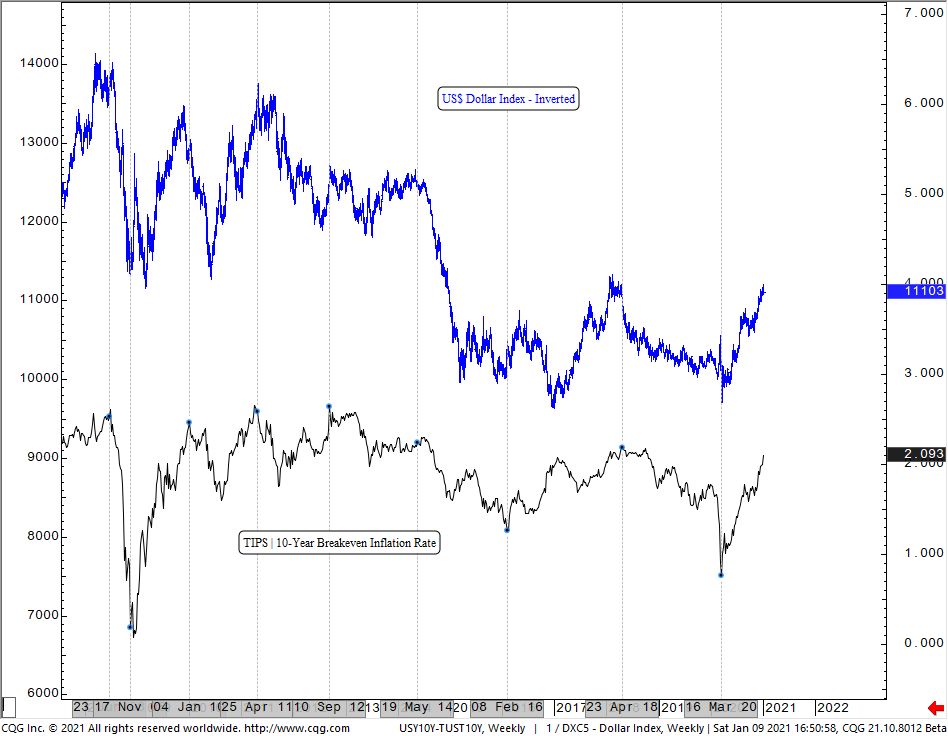

Fig #10 – US 10yr TIPS vs. US Dollar – Correlation Study by WaveTrack International

The US10yr breakeven inflation rate yield is also looking stretched to the upside – see fig’s #10 & #11.

Fig #11 – US10yr – USTIPS10yr – Yield Spread by WaveTrack International

Note the inverted correlation with the US$ dollar index which is already showing signs of beginning a multi-month upside risk-off correction. And from an Elliott Wave perspective, it has trended higher from the March ’20 COVID-19 lows of 0.558 into a five wave impulse pattern that is close to upside completion. A multi-month correction is about to begin, lasting several months before resuming its larger inflationary uptrend.

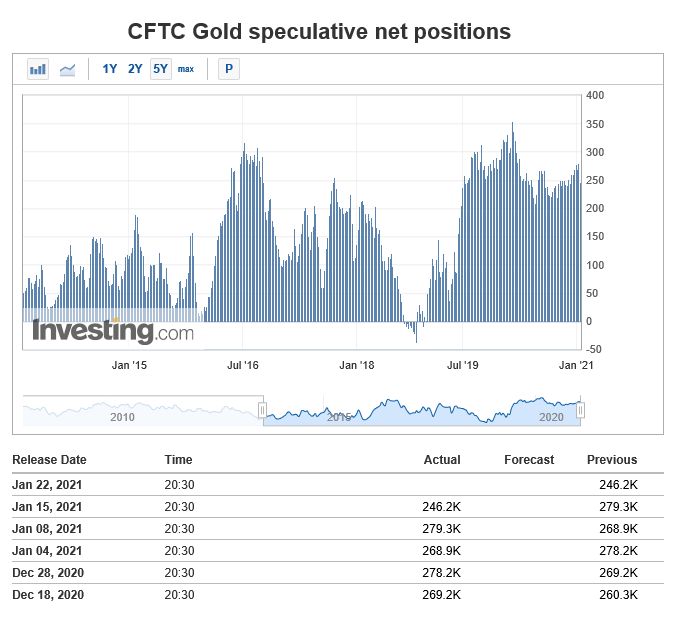

Gold

Fig #12 – CFTC Gold Speculative Net Positions – Source: Investing.com

Gold is an interesting commodity which attracted huge bullish interest last July/August. Although bullion prices traded up to new record highs last August, to 2072.12, prices have since begun counter-trend corrections. The latest CFTC shows how that peak coincided with peaks in net speculative long positioning although below record highs – see fig #12. Our cycle analysis also points towards more price declines through to July ’21 – see fig #13. And from an Elliott Wave perspective, gold is heading lower as wave (A) within a 4th wave correction but itself part of a five wave impulse uptrend that began from the Dec.’15 lows. That could keep gold range-trading for some time.

Fig #13 – Gold – Daily – Composite Cycle by WaveTrack International

Energy

In the energy sector, we’ve updated Crude/Brent oil showing how last year’s major declines ended super-cycle wave A from the all-time-highs of July ’08. Wave A is the first sequence in a very long-term triangle pattern where wave B is currently engaged in an ‘Inflation-Pop’ rally. However, we don’t expect wave B to reach new record highs because it’s showing early signs that it’s developing higher into a double zig zag pattern where the first cycle degree A-B-C zig zag is ending right now – so watch out for a multi-month correction!

Fig #14 – Largest Energy Sector Inflow since 2008 – Source: Bank of America

A correction seems possible when we look at the latest Bank of America survey – see fig #14. This shows the largest inflow into energy stocks since 2008 – okay that’s not the underlying commodity but the positive-correlation remains constant.

New Commodity 2021 Video – PART II/III

We’ve amassed over 90 commodity charts from our EW-Forecast database in this year’s Commodities 2021 video!! Each one provides a telling story into the way Elliott Wave price trends are developing in this next ‘INFLATION-POP’ phase of cycle development. We’re taking a look at some very specific patterns that span the entire SUPER-CYCLE, explaining why the super-cycle began from the GREAT DEPRESSION lows of 1932 and not from the lows of 1999 and how this ended in 2006-2008 and why the multi-decennial corrective downswing that began soon afterwards is taking the form of a very specific, but identifiable Elliott Wave pattern.

We invite you to take this next step in our financial journey with us – video subscription details are below – just follow the links and we’ll see you soon!

Most sincerely,

Peter Goodburn

Founder and Chief Elliott Wave Analyst

WaveTrack International

Commodities Video Part II

Contents: 92 charts

Time: 2 hours 25 mins.

• CRB-Cash index + Cycles

• US Dollar index + Cycles

• DB Agriculture Fund

• Copper + Cycles

• Aluminium

• Lead

• Zinc

• Nickel

• Tin

• XME Metals & Mining Index

• BHP-Billiton

• Antofagasta

• Anglo American

• Kazakhmys Copper

• Glencore

• Rio Tinto

• Teck Resources

• Vale

• Silver/Copper Correlation Study

• Gold + Cycles

• GDX Gold Miners Index

• Newmont Mining

• Amer Barrick Gold

• Agnico Eagle Mines

• AngloGold Ashanti

• Silver + Cycles

• XAU Gold/Silver Index

• Platinum

• Palladium

• Crude Oil + Cycles

• Brent Oil

• XOP Oil and Gas Index

• Natural Gas

How to buy the Commodity Video Outlook 2021

Simply contact us @ services@wavetrack.com to buy the COMMODITY Video Outlook 2021 for USD 48.00 (+ VAT where applicable) or alternatively our Triple Video Offer for USD 96.00 (+ VAT where applicable) – Review the content of WaveTrack Stock Indices Video PART I here. The last part of our Triple Video Series for Currencies and Interest Rates will be available approx. February/March 2021.

*(additional VAT may be added depending on your country – currently US, Canada, Asia have no added VAT but most European countries do)

We’re sure you’ll reap the benefits – don’t forget to contact us with any Elliott Wave questions – Peter is always keen to hear you views, queries and comments.

Visit us @ www.wavetrack.com

Stock Index Video Outlook – 2021 | PART I/III

by WaveTrack International| December 28, 2020 | 1 Comment

STOCK INDEX VIDEO OUTLOOK –

‘FINAL STAGE of the SECULAR-BULL UPTREND’

This report combines ELLIOTT WAVE with updated SENTIMENT & ECONOMIC INDICATOR STUDIES

We’re pleased to announce the publication of WaveTrack’s Annual 2021 video updates of medium-term ELLIOTT WAVE price-forecasts. Today’s release is PART I, STOCK INDEX VIDEO – Parts II & III will be published during January/February.

• PART I – STOCK INDICES

• PART II – COMMODITIES

• PART III – CURRENCIES & INTEREST RATES

Elliott Wave Stock Index Forecasts for 2021 – Summary

Fiscal & Monetary Stimulus Rescue

In last June’s mid-year report, COVID-19 Aftermath II – Secular-Bull Market Uptrend Resumes! we discussed how stock markets had collapsed, then staged a massive ‘V’-Shaped recovery. Whilst economists were still scratching their heads about the dislocation between the economic fall-out of a COVID-19 pandemic and exponential rises in stock markets, insiders were buying the markets basis one simple fact – central banks and governments around the world were embarking upon a historic, unprecedented path of fiscal and monetary stimulus as never seen before . And that means prices must rise! – and they did!

Global Fund Manager Survey

It was months later that Bank of America/Merrill Lynch’s Global Fund Manager Survey showed a sudden improvement in sentiment. Up until then, fund managers were still debating whether a recovery had begun at all! The majority said the rally was a brief one, with COVID-19 being the drag going forward. It wasn’t until after the northern-hemisphere annual summer holidays ended in mid-September that the realisation of a more sustained economic recovery began to filter into the mindset. By that time, the benchmark S&P 500 was higher by +64% per cent. Since then, a downswing followed by an upswing has taken the S&P 500 to a new record high. But even at today’s levels of 3733.00, that’s only +4% per cent gain since early-September. And yet more funds have been allocated into the markets over the last few months than at any other time since March.

Fig #1 – U.S. GDP – Quarterly – BEFORE COVID-19 – WaveTrack International

From an Elliott Wave perspective, you’d think that such an event as the COVID-19 pandemic would be a trigger for a secular bear market to begin. It’s certainly reverberated through many different economic statistics. A good example is the gyrational swings in the U.S. GDP (Gross Domestic Product) figures – see fig’s #1 & #2. Before COVID-19, annual GDP growth was around 2.10% per cent. And when the coronavirus struck and governments went into lock down mode, GDP collapsed to a low of minus -31.4% per cent, only to rebound later to +33.1% in the Q3 reporting. As you can see, these two swings are unprecedented. Even as far back as the 1940’s when the historical data began – crazy!

Fig #2 – U.S. GDP – Quarterly – AFTER COVID-19 – WaveTrack International

Fiscal and Monetary Stimulus

More impressive is the way central banks and governments have stepped in with an estimated $19.5 trillion dollars of fiscal and monetary stimulus in an attempt to shield their economies from the coronavirus pandemic. Record sums that take balance sheets and deficits to peacetime record highs. The sum equates to about 17% of an $87 trillion global economy. Leading the top-10 list is the United States with over $2.5 trillion pledged – see fig #3. Europe has since announced a new €1.5 trillion Euro-denominated package although spanning the next several years.

Fig #3 – Fiscal Power – Source: Goldman Sachs

U.S. M1 money supply has risen exponentially since March, growing by $2.2trn – see fig #4. As Elliott Wave analysts, whenever we see exponential rises like this, it almost always confirms the final sequence within a longer-term uptrend. Just like this one that began from the lowly-lows of the 1970’s. The trick is predicting how far and for how long it continues to rise before forming a major peak, then declining just as quickly in the subsequent years to form that all-so-familiar parabolic bell-shaped curve.

Fig #4 – US – Money Supply Growth – Source: Federal Reserve

I think we have a pretty good idea of what conditions will end the current asset price rise and an indication of when that peak occurs.

Dow Jones On-Course for Long-Term 40,000-42,000 Upside Targets

Back in November/December 2014, six years ago, the Dow was trading at 17817.00, approaching original upside targets forecast back in 2010. But this secular-bull peak wasn’t aligned to the completion of corresponding ‘Inflation-Pop’ upside targets for Emerging Market indices and key Commodities like Copper and Crude Oil.

This was a big hint that the secular-bull uptrend in the Dow Jones (DJIA) and other developed market indices were far from complete. Further analysis revealed some amazing Fibonacci-Price-Ratio (FPR) ‘proportion’ values across the entire history of its major five wave impulse uptrend dating back to the Great Depression lows of 1932 – see fig #5. They coalesced towards Dow 40,000-42,000!

Fig #5 – Dow Jones 30 – Quarterly – WaveTrack International

The secular-bull uptrend was labelled unfolding into a cycle degree pattern, 1-2-3-4-5. Extending waves 1-4 by a fib. 161.8% ratio projected ultimate upside targets for wave 5 towards 41116.70+/-,

1 (40.50) – 4 (570.00) x 161.8% = 5 @ 41116.70

Furthermore, subdividing cycle wave 5 into primary degree, 1-2-3-4-5, a fib-price-ratio convergence forms at 41982.10+/- where primary wave 5 unfolds by a fib. 61.8% correlative ratio of waves 1-3,

1 (570.00) – 3 (11750.30) x 61.8% = 5 @ 41982.10

Subdividing primary wave 5 into intermediate degree, (1)-(2)-(3)-(4)-(5) also provides ultimate upside targets for wave (5) towards 39207.00+/- derived by extending wave (1) by a fib. 161.8% ratio,

(1) [6470.00-12391.30] x 161.8% = (5) @ 39207.00

These three upside targets average out at 40768.60+/-

And so, proportionally, symmetrically and harmonically, Dow 40-42k remains to this day, a very realistic probability of being reached before the secular-bull uptrend is completed.

Timing the ‘Inflation-Pop’ Peak

Cycle analysis has since shown a 94-year cycle peak due in late-2023/early-2024 that has our attention in providing the timing for the ‘Inflation-Pop’ bubble-burst. See June’s report or this new, updated PART I STOCK INDICES annual report/video.

US$ Dollar Outlook

One contributor that’s expected to drive asset values significantly higher over the few years is a weakening US$ dollar – see fig #6.

Fig #6 – US Dollar Index – Cycle – Monthly – WaveTrack International

There’s a distinct 15.6-year cycle recurrence for the US$ dollar index which has signalled the various peaks and troughs over the past several decades. However, in our original cycle analysis, the 15.6-year model showed the dollar’s decline into its next ‘trough’ due in 2023/24. But we wonder if there’s enough time for a -45% decline basis our Elliott Wave analysis where cycle wave C declines bottom around 49.35+/– see fig #7?

Fig #7 – US Dollar Index – Monthly – WaveTrack International

It’s possible to lengthen the cycle interval to 16.25 years, which connects the cycle-troughs together in a more synchronous rhythm. That would stretch the next cycle-trough into Oct.’27. That would allow more time for the dollar’s decline to test 49.35+/-. It might also lengthen the stock market secular-bull uptrend too?

Shorter-Term – Risk-Off During Q1 ‘21

Shorter-term analysis suggests the post-COVID-19 risk-on advances in global stock markets and commodities is about to take a rest. One hint comes from the oversold condition in the US$ dollar – see fig #8. In this chart from Bloomberg, asset managers are shown with huge net-short positioning, at record levels. That will almost certainly trigger a relief rally in the dollar soon, indicating the stock market will undergo a severe correction during Q1 2021, contrary to consensus opinion.

Fig #8 – Bearing Down – Source: Bloomberg

The US$ dollar index is approaching the downside completion of a five wave impulse pattern from March’s COVID-19 peak of 102.99 where downside targets already being tested at 89.73 but potentially extending to 88.21+/- prior to a sustained counter-trend, multi-month advance – see fig #9. This would suggest a period of risk-off during Q1 ’21.

Fig #9 – US Dollar Index – 720 mins. – WaveTrack International

Stock Index and Sentiment

Citigroup’s Market Sentiment index is confirming the same risk-off period is about to begin across New Year – see fig #10. It advanced to a fresh record high at 1.65 vs 1.61 last week and 1.10 in the week prior. Anything above .40 is considered euphoric and from a contrarian perspective, is screaming out for a stock market correction.

Fig #10 – Market Sentiment – Source: Citigroup

Earlier last month, Bank of America/Merrill Lynch’s GFM survey showed investor optimism had sky-rocketed over the past months, since September, where levels are at 46% per cent whilst hedge funds’ equity exposure remains high at 41% per cent – see fig #11.

Fig #11 – November Survey shows FMS Investor Optimism on Stocks Skyrocketed

S&P 500 – Short-Term Correction Q1 ‘21

The S&P 500’s advance from the March COVID-19 low of 2174.00 has unfolded into a five wave impulse pattern, labelled minor wave i. one within intermediate wave (5)’s ongoing uptrend. Subdividing into minute degree, 1-2-3-4-5, wave 5 completed into the early-September high of 3587.00. This was slightly higher than upside targets of 3511.00+/- and just below 3595.00+/- derived by extending wave 1 by a fib. 161.8% ratio – see fig #12.

Fig #12 – E-Mini S&P500 Futures – 960 mins. – WaveTrack International

Minor wave ii. two’s correction is already underway, unfolding into a three wave a-b-c expanding flat pattern. This allows a modest higher-high in the second sequence prior to a third wave decline. This explains why the S&P has since traded up to 3733.00. Applying Elliott’s guideline that corrections fall back towards ‘fourth wave preceding degree’, minimum downside targets are towards the area of minute wave 4’s low of 2923.75. That translates into a heft decline of around -20% per cent during Q1 ’21, very much against the consensus view.

European Indices / Emerging Markets + Asia – Australia – Japan

An important aspect related to the next surge higher is the Elliott Wave pattern development of European and Asian indices. These have very different patterns in upside progress from the financial-crisis lows of 2008/09. But they do conform to the ‘Inflation-Pop’ schematic of zig zags or double zig zag advances over multiple decade periods.

If you’re an asset manager located in Europe or Asia, it’s imperative to understand how these benchmark indices fit into the larger U.S. picture! This latest annual 2021 report takes an in-depth look at the price-projections for the MSCI EM index plus many more EM and ASIAN indices.

Annual 2021 Outlook – Report/Video

Our annual 2021 Stock Index report/video is PART I of a three-part trilogy series of Elliott Wave analysis and the outlook into the final stages of the secular-bull ‘Inflation-Pop’ cycle.

We’ll be taking a close introspective look across many U.S. indices, the large-cap and small-cap trends, but also across many different sectors too including the FANGS+ index, U.S./European Banks, Biotechnology, Technology and many more – we’re also updating some fascinating Elliott Wave counts for several economic data points too, including Consumer Sentiment, Consumer Confidence, Price to Book Ratio, Price-Sales Ratio! It all adds-up to one thing – huge gains over the next few years!

New Stock Index 2021 Video – PART I/III

This ANNUAL 2021 VIDEO UPDATE for STOCK INDICES is like nothing you’ve seen anywhere else in the world – it’s unique to WaveTrack International, how we foresee trends developing through the lens of Elliott Wave Principle (EWP) and how its forecasts correlate with Cycles, Sentiment extremes and Economic data trends.

We invite you to take this next step in our financial journey with us – video subscription details are below – just follow the links and we’ll see you soon!

Most sincerely,

Peter Goodburn

Founder and Chief Elliott Wave Analyst

WaveTrack International

Contents Stock Index Video Outlook 2021

Charts: 84 | Video: 1 hour 59 mins.

Read more «Stock Index Video Outlook – 2021 | PART I/III»

The EW-Navigator

by WaveTrack International| November 23, 2020 | No Comments

U.S./European stock Indices set for Further Declines into Year-End – Underperformance in Technology – Emerging Markets to Pull Lower – Energy Stocks on Buy Signals + Eurozone Banks – US$ Dollar Heading Higher – Interest Rates Pulling Lower within Uptrend

The world is still adjusting to the uncertainties of this year’s COVID-19 pandemic. Especially, its effect on economic globalisation, second-phase lockdowns, huge rises in corporate defaults, and of course, the results of a U.S. election. Within that, risks of an uprising of popularism over mandatory vaccination and the withdrawal of civil rights are seemingly put aside as the financial world gorges on another round of central bank liquidity, driving asset prices significantly higher from the March lows. Back in 2011, the Elliott Wave Navigator report created a new term to describe the effects of a post-financial-crisis recovery, the ‘Inflation-Pop’. Almost a decade later, billionaire mavericks controlling family offices, hedge funds, and some of the world’s largest asset managers are now uttering the same words, ‘Inflation’ – ‘Inflationary’. What was it that inspired that long-range forecast back in 2011? And what effects does it hold in store for the coming decade as 2021 approaches?

This month’s report begins by taking a look at the current location of the U.S. stock markets’ price-development since last March, highlighting shorter-term risks supported by the very latest cycle analysis.

There’s good reason to forecast a 2-month correction unfolding from September’s/current highs especially when you consider just how bullish sentiment is right now, at least from a contrarian standpoint. The latest Global Fund Manager Survey from Bank of America/Merrill Lynch shows investors are in ‘full-bull’ mode as they push more funds into emerging markets, small-cap stocks, and the banking sector on hopes a COVID-19 vaccine will turn around these hard-hit market sectors.

Fig #1 – Global FMS – Source: Bloomberg

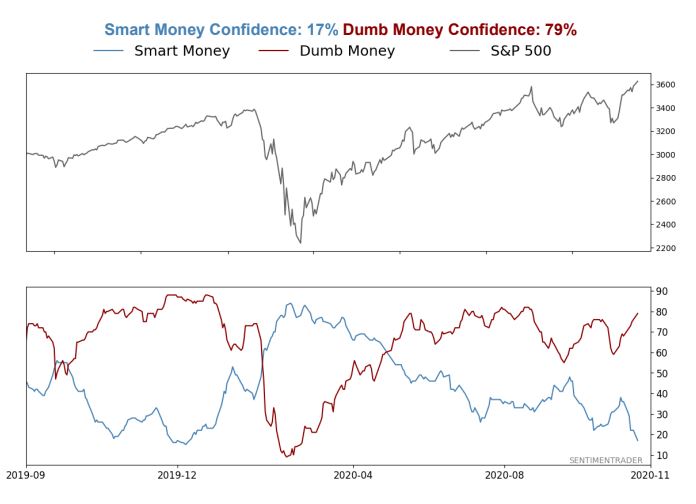

Sentiment is the most stretched since January as highlighted in the latest SentimenTrader report. The spread between ‘Smart Money’ and ‘Dumb Money’ confidence has eroded to minus -62% on their scale, one of the widest since data began recording in 1999.

Fig #2 – Smart Money Confidence

Moving on, this month’s report updates the Nasdaq 100 and FANG+ index with price-directional forecasts through to year-end. Our monthly U.S. sector analysis updates the Elliott Wave pattern development of XLK-Technology, XLY-Consumer Discretionary, XLB-Materials, XLF-Financials, and two energy contracts, XLE-Energy and XOP Oil & Gas.